Written by: Jay Yi, MBA; Edited by: Chris Thompson, CFA, MBA, P.Eng

eResearch | Netflix, Inc. (NASDAQ: NFLX; LSE: 0QYI; DE: NFC) beat analysts’ earnings expectations for Q3/2019, but weak guidance, increased competition, and continued negative operating cash flows has fueled a stock price decline of almost 30% from its peak in July and is now flat year-to-date.

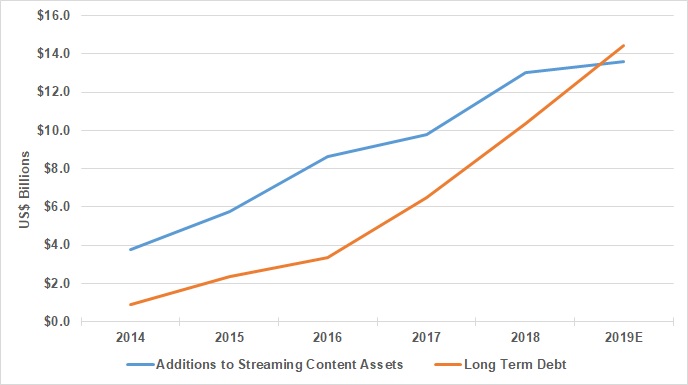

In Q3/2019, Netflix reported US$5.4 billion in revenue and US$665 million in net income; however, it had US$501 million in negative operating cash flows, as it capitalized US$3.6 billion in costs of “additions to streaming content assets” in the quarter, significantly reducing booked expenses as it invests heavily into creating and acquiring content. To support the capital expenditure for the additions to streaming content assets, Netflix has been increasing its long-term debt which has resulted in a 48% increase in interest expense year-over-year.

After releasing earnings, Netflix announced a US$2 billion debt financing as it continues to raise funds for investment in content acquisition, production and development, and working capital. Only six months ago, Netflix raised US$2.2 billion for content creation needs.

As illustrated in the chart below, Netflix is borrowing more money to buy and create content, but debt is exceeding content assets additions.

Additions to Streaming Content Assets and Long-Term Debt

By adding only 6.7 million new subscribers in the quarter, Netflix also missed its guidance of adding seven million paid members. Last quarter, Netflix also missed guidance when it reported a loss in paid subscriptions in the U.S. for the first time and added only 2.7 million international subscribers, almost half of Netflix’s guidance. Guidance for next quarter expects a further decrease in the growth rate of paid subscription memberships.

This is a reality check for Netflix who has shown impressive growth in the recent past. As the competitive landscape changes due to new entrants, Netflix may no longer have the pricing power to act as the price maker and is also forced to pay more for content licensing. This forces Netflix to raise larger amounts of debt to develop more of its own content assets as well as pay higher licencing fees as it competes with other streaming offerings.

Netflix Q3/2019 Earnings Highlights

- Revenue of US$5.4 billion, a 31% increase year-over-year, attributed to a 6.7 million increase in paid subscription memberships, a 21.4% increase year-over-year.

- Net Income of US$665 million, a 65% increase year-over-year.

- Interest expense increased to US$160 million, a 48% increase year-over-year, due to aggressive fund raising for content development and acquisition.

- Operating cash flow loss of US$501 million mainly due to an increase in additions to streaming content assets of US$3.6 billion, a 13% increase year-over-year.

- Current content liabilities of US$4.8 billion, a 4% increase year-over-year, and non-current content liabilities of US$3.4 billion, a 9% decrease year-over-year.

- Long term debt of US$12.4 billion, a 20% increase year-over-year, due to fundraising for acquisitions and content creation.

- Cash and cash equivalents of US$4.4 billion, mainly from loans.

As competitors such as Disney and AT&T develop their own subscription-based streaming platforms, Netflix is raising capital to focus on creating its own content in an effort to build a competitive advantage.

In 2019, Netflix is expected to increase spending on proprietary content creation to US$15 billion, after having already increased content spending by 35% last year to US$12 billion, but it is in a disadvantage against competitors who are large conglomerates with massive amounts of capital.

Netflix plans to be the leader in the subscription-based streaming industry, but will they be able to sustain operations with increasing debt levels, pricing wars, and slowing membership subscription growth?

//

Netflix, Inc. (NASDAQ: NFLX; LSE: 0QYI; DE: NFC)

- NetflixInvestor.com

- Headquartered in California, United States, Netflix is a media-services provider with over 140 million paid subscribers for their streaming platform. Since 2012, in preparation for competition to their streaming platform, Netflix has taken a more active role as a producer and distributor for both movies and TV shows.

- Netflix currently trades at US$266.69 per share with a market capitalization of US$116.8 billion.

//

TV Streaming Services

| Amazon | Amazon Prime Video | $12.99/month; part of Amazon Prime |

| Amazon | IMDb TV | Free ad supported |

| Apple | Apple TV+ | $5.99/month |

| AT&T | AT&T TV | $9.99/month |

| Discovery/BBC | Discovery/BBC | $4.99/month |

| Disney | Disney+ | $6.99/month or $69.99/year |

| YouTube TV | $50/month | |

| HBO | HBO Now | $14.99/month |

| HBO | HBO Max | $16.99/month |

| Hulu | Hulu + Live TV | $5.99-$45/month |

| NBCUniversal | NBCUniversal/Peacock | Free (with ads) + $15/month |

| Netflix | Netflix | $9.99-$15.99/month |

| Roku | Roku Channel | Free + Premium Paid TV |

| Sling TV | Sling TV | $25-$40/month |

| Sony | PlayStation Vue | $49.99-$84.99/month |

| Walmart | VUDU | Free (with ads), rent or buy TV shows and movies |

Source: eResearch Corp.; all figures in US dollars