eResearch is pleased to publish an Update Equity Research Report on DATA Communications Management Corp. (TSX: DCM | OTC: DCMDF).

We are maintaining a Buy rating and a one-year price target of $6.90.

You can download our 15-page Equity Research Report by clicking on the following link: eR-DCM-2023_11_13_UR-2023-Q3_v06-FINAL

Company Overview

DCM is a Canadian-based provider of marketing and business communication solutions to companies in North America. Its technology-enabled content and workflow management capabilities solve the complex branding, communications, logistics, and regulatory requirements of leading enterprises so its customers can accomplish more in less time. Its services include printing, data & content management, labels & asset tracking, location-specific marketing, and multimedia campaign management.

Company Update:

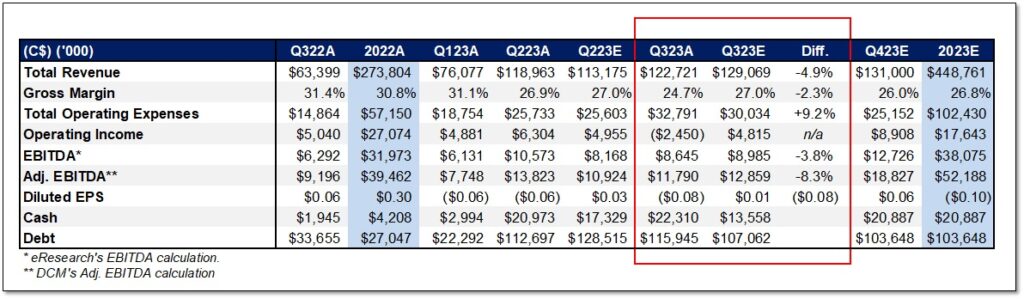

- On November 8, 2023, DCM reported Q3/2023 financial results with Revenue up 93.6% to $122.7 million but slightly lower than our estimate of $129.1 million due to seasonality. Adjusted EBITDA in the quarter was $11.8M, an increase of 28.2% from $9.2 million in the same quarter last year. The Revenue and EBITDA growth were mainly attributable to the acquisition of Moore Canada Corporation (MCC), which closed in Q2/2023.

- The Company reported Gross Profit of $30.3 million in Q3/2023, up 52.4% from $19.9 million in the same quarter last year. In Q3/2023, Gross Margin as a percentage of revenue was 24.7%, down 6.7% from 31.4% in Q3/2022, and lower than our estimate of 27.0%. The decline in gross margin is attributed to MCC’s lower average gross profit margins, which lowered the overall gross profit margin of DCM. Despite this, DCM reported that it has developed a strategic plan to restore the combined gross profit margins to at least 30%, the level DCM was at before the acquisition.

- The Company reported a Loss of $4.2 million in Q3/2023, down from a Profit of $2.8 million in Q3/2022. Basic and Diluted EPS in the quarter was negative $0.08 compared to $0.06 in the same quarter last year. The decline in Net Income can be attributed to several factors, including restructuring costs of $7.0 million, one-time acquisition and integration expenses of $0.2 million, net fair value losses on financial liabilities of $0.7 million, and an increase in interest expenses related to the higher debt levels undertaken to finance the MCC See the “Merger Update” section of the report, for additional details.

FIGURE 1: DCM’s Q3/2023 Results Compared to eResearch Estimates

- As of September 30, 2023, DCM had $22.3 million in cash. Although it aims to maintain a low cash balance to reduce the borrowing charges under its credit facilities, due to the MCC acquisition, the Company is currently carrying a higher-than-normal cash balance. At the end of the quarter, the Company’s Total Debt, excluding the Lease Liabilities, stood at $115.9 million, up 2.9% from $112.7 million in Q2/2023, due to an increase in Working Capital requirements. Net Debt, excluding Lease Liabilities, ended the quarter at $93.6 million. DCM reiterated its focus on debt reduction as a key strategic priority.

- DCM has revised its forecast for anticipated merger synergies to between $30 million to $35 million over the next 18 to 24 months, up from the previous range of $25 million to $30 million with annualized savings of $17.5 million expected in 2024.

- We maintain that this transaction significantly bolsters DCM‘s growth potential and capabilities, offering economies of scale along with an expanded range of products, services, and technological advancements.

- We estimate DCM could generate over $60 million of EBITDA in 2024, which could be allocated towards debt reduction, dividend distribution, or exploring further acquisition opportunities.

FIGURE 2: DCM’s Revenue Momentum Continued in Q3/2023

Financial Analysis & Valuation:

- We updated our model with the DCM’s recent financials and adjusted our model to include further deal synergies but slightly lower margins.

- We estimate an equal-weighted price target of $6.90 based on a DCF valuation ($9.31/share), a Revenue Multiple valuation ($6.17/share), and an EBITDA Multiple valuation ($5.10/share).

We are maintaining a Buy rating and a one-year price target of $6.90.

You can download our 15-page Equity Research Report by clicking on the following link: eR-DCM-2023_11_13_UR-2023-Q3_v06-FINAL

Other DCM Research Reports:

- Update Report (August 17, 2023): DCM Acquisition Provides 75% Revenue Jump & Cash Flow Growth as Merger Synergies Drop to the Bottom Line

- Update Report (June 14, 2023): DCM and MCC Merger Closes and Leaps Forward with $26.1M Financing & $23.1M Facility Sale

- Update Report (March 10, 2023): Strategic Merger Between DCM and RRD Canada Sparks Industry Consolidation with Beneficial Synergies

- Update Report (November 11, 2022): Double-Digit Quarterly Revenue Growth Continues Positive Business Momentum and Strong EBITDA in Q3/2023

- Update Report (August 23, 2022): Strong Business Momentum Continues with Y/Y Revenue Growth of Over 23% in Q2/2022

- Update Report (July 29, 2022): DCM Corporate Strategy Drives Business Transformation with Q1/2022 Producing Largest Revenue Growth in 4 Years

- Update Report (April 29, 2022): DCM’s Quarterly (Q4/2021) Revenue Improves Y/Y as a Sign of COVID Impacts Easing

- Update Report (November 24, 2021): DCM Q3 Financials In-line as Consolidation Improves Cash Flow

- Initiation Report (August 16, 2021): Digital-First Strategy and Tactical Consolidation Drives EBITDA Growth at DCM

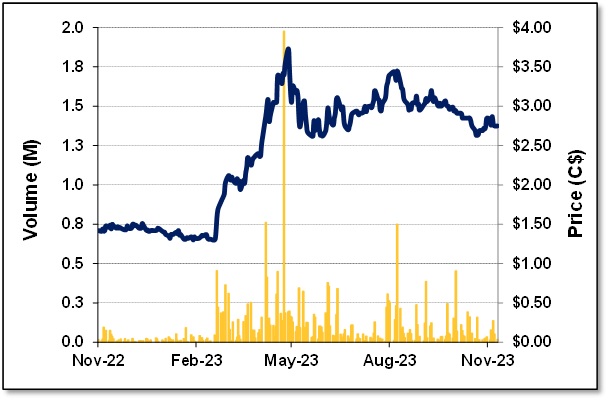

FIGURE 3: One-Year Stock Chart

Notes: All numbers are in CAD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.