Written by: Jay Yi, MBA; Edited by: Chris Thompson, CFA, MBA, P.Eng

![]()

![]() eResearch | On September 9, 2019, the Board of Directors for AT&T Inc. (NYSE: T; LSE: 0QZ1) received a letter from Elliott Associates, L.P., an investment firm with a US$3.2 billion stake in the Company, expressing concerns about past management decisions but also stating that AT&T has potential to nearby double its stock price by 2021 through refocusing its strategy.

eResearch | On September 9, 2019, the Board of Directors for AT&T Inc. (NYSE: T; LSE: 0QZ1) received a letter from Elliott Associates, L.P., an investment firm with a US$3.2 billion stake in the Company, expressing concerns about past management decisions but also stating that AT&T has potential to nearby double its stock price by 2021 through refocusing its strategy.

Click on the link to view a copy of the letter: Elliotts-Letter-to-ATT_09092019

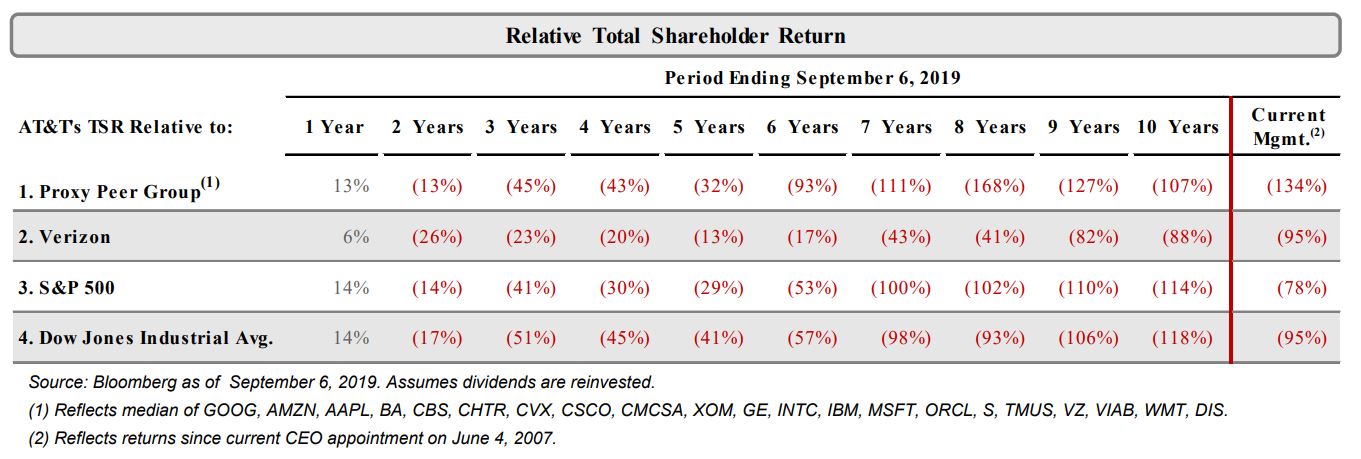

AT&T has recorded weak performance over the past 10 years and has underperformed the S&P 500 Index by over 150%. The Company’s Total Shareholder Return (TSR) significantly lacked in relation to not just the S&P 500 but also to its competitor Verizon who outperformed AT&T by 88% over a 10-year period.

Elliott explained in the letter that they believe the Company’s consecutive inadequacies can be categorized into two baskets, (1) strategic setbacks and (2) operational underperformance.

1. Strategic Setbacks: AT&T built its early success through focusing on a niche growth strategy within the wireline and wireless industries in the U.S., and in between 1997 and 2007, the Company became a market leader through acquiring numerous competitors. This strategy was set back recently in the past decade as AT&T invested a total of approximately US$200 billion in acquiring companies and business lines that were not in alignment with AT&T’s core competencies, and recently the Company made a push into the Mexican wireless market. Highlighted below are AT&T’s three major strategic setbacks:

![]()

![]() In 2011, AT&T attempted to force a takeover acquisition of T-Mobile, the fourth-place competitor in the industry at the time, for US$39 billion, but the deal was quickly shut down by the government due to concerns over monopoly. AT&T ended up paying a break-up fee in the form of spectrum as it had to provide T-Mobile with a seven-year roaming deal that eventually helped T-Mobile become a valiant competitor today.

In 2011, AT&T attempted to force a takeover acquisition of T-Mobile, the fourth-place competitor in the industry at the time, for US$39 billion, but the deal was quickly shut down by the government due to concerns over monopoly. AT&T ended up paying a break-up fee in the form of spectrum as it had to provide T-Mobile with a seven-year roaming deal that eventually helped T-Mobile become a valiant competitor today.

![]()

![]() In 2014, AT&T made is first significant investment into a divergent business line with a US$67 billion acquisition of DirecTV, to become the largest pay TV operator in the U.S. Since the acquisition, the TV industry has been on a continuous decline as it is disrupted by streaming platforms such as Netflix and the Disney’s soon to be released Disney +

In 2014, AT&T made is first significant investment into a divergent business line with a US$67 billion acquisition of DirecTV, to become the largest pay TV operator in the U.S. Since the acquisition, the TV industry has been on a continuous decline as it is disrupted by streaming platforms such as Netflix and the Disney’s soon to be released Disney +

![]()

![]() In 2016, AT&T made its largest investment yet with a US$85 billion acquisition of Time Warner (now named Warner Media), a valuable franchise with a premium collection of media assets. It has been three years since the signing of the acquisition, but AT&T has yet to paint a clear picture on its strategy or intent for value creation with Time Warner.

In 2016, AT&T made its largest investment yet with a US$85 billion acquisition of Time Warner (now named Warner Media), a valuable franchise with a premium collection of media assets. It has been three years since the signing of the acquisition, but AT&T has yet to paint a clear picture on its strategy or intent for value creation with Time Warner.

2. Operational Underperformance: The Company started to divest its focus into different industries which affected the execution of AT&T’s core business in the wireless industry as the Company failed to (i) take full advantage of exclusive distribution rights for the iPhone in 2007 due to problems scaling infrastructure, (ii) build its brand as a fast network due to slow execution of 4G LTE implementation, and (iii) differentiate a value proposition as competitor Verizon took lead of the premium market and T-Mobile took lead of the discount market.

Though AT&T has struggled executing in the past with poorly made decisions, the Company has significant media assets that are irreplaceable in the market with enormous earning powers that have the ability to win key markets. Elliot confidently believes that with AT&T’s assets, there is significant opportunity to execute and lead in wireless with its 5G network and entertainment with its HBO Max streaming service.

To grasp opportunities and retake a leading market position, Elliott outlined goals and strategies in the “Activating AT&T Plan”, which includes (1) Improved Strategic Focus, (2) Significant Operational Improvements, (3) Formal Capital Allocation Framework, and (4) Enhanced Leadership and Oversight.

Overall, Elliott wants AT&T to find appropriate leadership that can improve operations by divesting non-core assets that are creating redundancies and noise, paying down 50% of debt with a <2x leverage ratio, and increasing EBITDA margins through consolidating operations and expenses. The Activating AT&T Plan believes it can increase AT&T’s share price to US$60 compared to the US$37.19 it is trading today.

//

AT&T Inc. (NYSE: T; LSE: 0QZ1)

Headquartered in Texas, United States, AT&T is the word’s largest mobile telephone service company. In 2018, it acquired Warner Media for US$85 billion, to utilize their HBO streaming platform to compete against Netflix. AT&T currently trades at US$37.21 with a market capitalization of US$271.9 billion

//