Diablillos contains multiple, near-surface deposits, including Oculto, which is a high-sulphidation epithermal silver-gold deposit. The property is situated in an established mining camp that contains several borate and lithium mining operations.

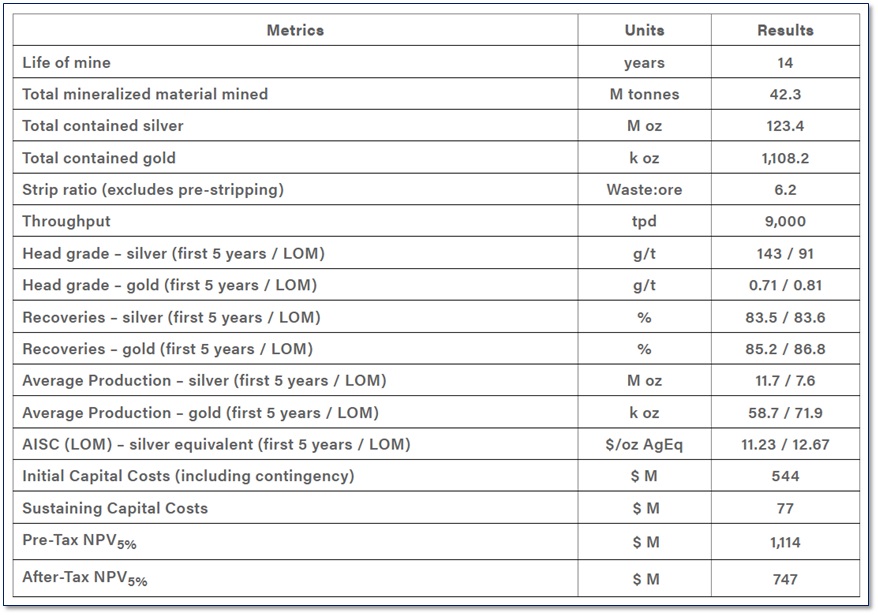

The project boasts a Proven and Probable reserve estimated at 42.3 million tonnes grading 91 grams per tonne (g/t) silver and 0.81 g/t gold. This would translate into 124 million silver ounces and 1.1 million ounces of gold. In addition, Diablillos has a Measured and Indicated resource estimated at 258 million silver-equivalent ounces.

At its La Coipita project in Argentina, AbraSilver has a joint venture agreement with Teck Resources (TSX: TECK.B). The project contains multiple porphyry copper-gold drill targets and Teck can earn up to an 80% interest in the project by funding up to US$20 million in exploration and some additional payments.

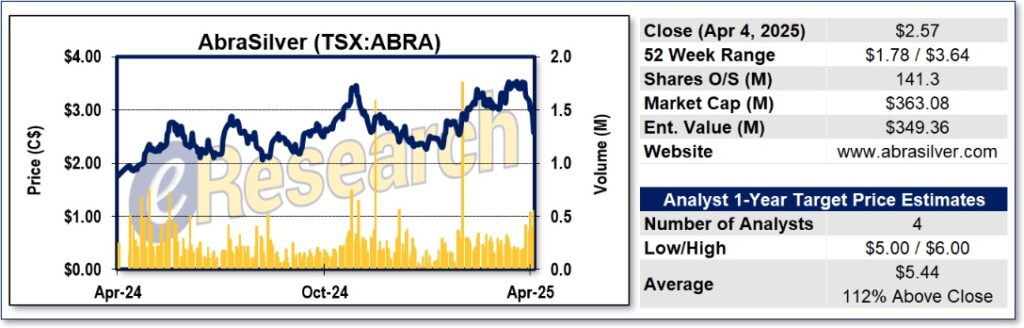

Stock Price Reacting Positively to Recent News

AbraSilver’s stock price has gained 414%, to its current price of around $2.57 per share, since we first began following the company about five years ago, including a 47% surge over the past year.

There have been a few catalysts propelling AbraSilver’s share price higher over the past several weeks. On December 3, 2024, the company released the results of an updated Pre-Feasibility Study (PFS) for its Diablillos project.

On February 12, 2025, AbraSilver announced it closed an equity financing of $28.5 million at $2.55 per share. Combined with a previously reported $30 million public offering, the company raised about $58.5 million in recent financings. Proceeds from the combined offerings are expected to be deployed primarily to speed up the advancement of the Diablillos project.

Notably, Kinross Gold (TSX: K) bought nearly 1.1 million units of AbraSilver Resource’s recent placement and now has an approximately 4% equity stake in the company. Already a shareholder, billionaire mining financier Eric Sprott also bought into a recent financing and now owns about 9.3% of AbraSilver.

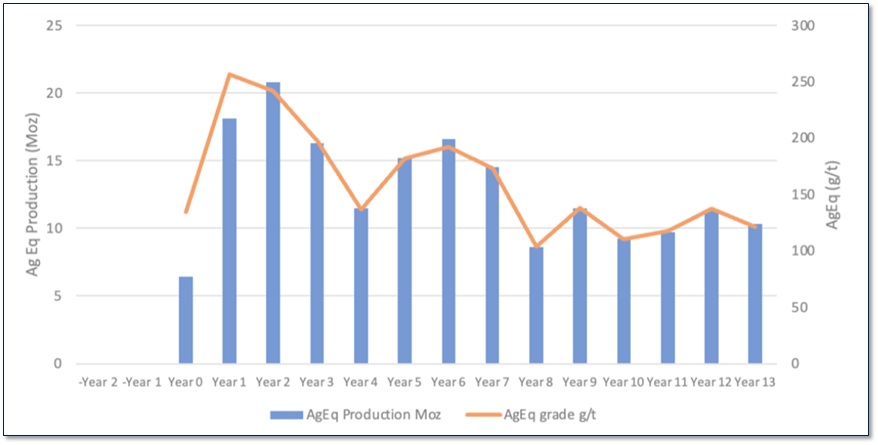

FIGURE 1: Annual Silver Equivalent Production and Grade Profile

Diablillos Project PFS Economics

The PFS estimates an after-tax Net Present Value (NPV), base case, of US$747 million, or $1.046 billion in Canadian dollars, using a discount rate of 5% per year, an Internal Rate of Return (IRR) of 27.6%, and a payback period of two years. The NPV used a gold price assumption of US$2,050 per ounce and a US$25.50 per ounce silver price. Thus, the economics of the project would improve significantly at the current gold price of more than US$3,000 an ounce and a silver price that now exceeds US$30.

The PFS also estimates an average annual silver and gold production of 13.4 million silver-equivalent ounces over a mine life of 14 years, consisting of 7.6 million ounces of silver and 72,000 ounces of gold. During the first five years of full production, output is expected to average 16.4 million silver-equivalent ounces per year, which would be comprised of 11.7 million silver ounces and 59,000 ounces of gold.

AbraSilver’s all-in sustaining cash costs of production is expected to average US$12.67 per silver-equivalent ounce over the life of the mine, with that figure falling to US$11.23 during the first five years of full production.

However, the initial capital expenditure is estimated at US$544 million, with an additional US$77 million in sustaining capital over the life of the mine. So there still is a lot more work and financing to be done to get this project ready for production.

FIGURE 2: Summary of Project Economics

Final Thoughts

With strong economics, a growing resource base, and backing from industry players like Kinross Gold and Eric Sprott, AbraSilver is positioning itself to become a mid-tier silver-gold producer in a jurisdiction with a rich mining history.

Figure 1: ABRA 1-Year Stock Chart

Other reports on AbraSilver (fka AbraPlata):

Notes: All numbers in CAD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.