eResearch is pleased to publish a 23-page Update Equity Research Report on Silver Bullet Mines Corp. (TSXV: SBMI | OTC: SBMCF).

We are maintaining our Speculative Buy rating and increasing our one-year price target to $0.40 due to the Transition to Multi-Asset Producer.

You can download our 23-page Equity Research Report by clicking on the following link: eResearch-SBMI-UR-2025_12_08-FINAL

Company Overview

Silver Bullet Mines Corp. (“SBMI” or “the Company”) is a Canadian-based silver and gold exploration and development company. SBMI‘s primary asset is the Black Diamond (“BD”) Property, located near Globe, Arizona, which includes several past producers, focusing primarily on the silver-copper veins of the area, including the Buckeye, McMorris, Richmond, and Jumbo.

In addition to the BD Property, SBMI has acquired the King Tut and Super Champ properties from third parties, both of which now serve as important sources of near-term mill feed.

SBMI commenced production at Buckeye in 2022, but it has begun generating revenue by processing mineralized material from the King Tut and Super Champ properties at its mill in Globe, Arizona, with initial concentrate sales completed in 2025. These operations position the Company as an emerging small-scale producer.

SBMI is also advancing its Washington Mine in Idaho, a historical silver and gold mine undergoing underground development and bulk-sample preparation. The Company is working toward securing final processing arrangements.

REPORT HIGHLIGHTS

RECENT COMPANY UPDATES:

- First Concentrate Sales: SBMI achieved its first commercial sales in 2025, shipping concentrate from both the King Tut gold and Super Champ silver mines under its offtake arrangement with a U.S. buyer, marking SBMI’s transition into a revenue-generating company.

- Arizona Advancements: At King Tut, underground development and test milling confirmed high-grade gold mineralization with concentrate grades of 38 oz/ton gold at 90% recovery. Super Champ development continued with additional high-grade silver sampling and expanded access.

- Washington Mine Progress: In Idaho, SBMI advanced the Washington Mine by extending and enlarging the main adit to 190 feet, establishing drill stations, and confirming several historical high-grade zones. The Company seeks to secure a third-party processor for milling.

- Strengthened Financial Position: SBMI completed three equity financings in 2025, including two priced at premiums to market, raising a total of approximately $4.9 million. Several debenture balances were converted or retired, improving the Company’s balance sheet ahead of expanded production plans.

INVESTMENT THESIS:

- SBMI made measurable operational progress over the past year. The Company generated its first concentrate sales, advanced two silver and gold projects, acquired and advanced a third asset on favourable terms, and maintained consistent mill operations.

- The investment thesis now rests on near-term gold production from King Tut, incremental silver contributions from Super Champ, and continued development at the Washington Mine.

- Strategic financings, many priced at premiums to market, provided capital to support mine development and mill improvements.

FINANCIAL ANALYSIS & VALUATION:

- We are maintaining a Speculative Buy Rating on SBMI and increasing our one-year Price Target to $0.40.

- Our valuation is based on forward-looking cash flow estimates derived from estimated production at the Company’s three active projects (King Tut and Super Champ in Arizona, and the Washington Mine in Idaho) and assigning a $5 million value to the McMorris Mine and other legacy properties.

- Arizona operations are projected to generate US$4.86 million in revenue over 12 months. It assumes the Globe Mill processes approximately 6,000 tons per year, with the majority of feed coming from King Tut at 0.5 oz/ton gold, with some feed from Super Champ at 20 oz/ton silver, at prices of US$3,800/oz gold and US$45/oz silver, with 50% margins.

- In Idaho, operations are projected to contribute US$3.65 million through two 2,500 bulk samples (totaling 5,000 tons) at 30 oz/ton silver, processed by a third party at 60% margins and US$45/oz silver.

- Adjusting for estimated corporate and development expenses and net debt, and using a 7.5x cash flow multiple, produces an equity value of $69.18 million. Dividing by an estimated 172.9 million fully diluted shares supports a 12-month target price of $0.40 per share.

We are maintaining our Speculative Buy rating and increasing our one-year price target to $0.40 due to the Transition to Multi-Asset Producer.

You can download our 23-page Equity Research Report by clicking on the following link: eResearch-SBMI-UR-2025_12_08-FINAL

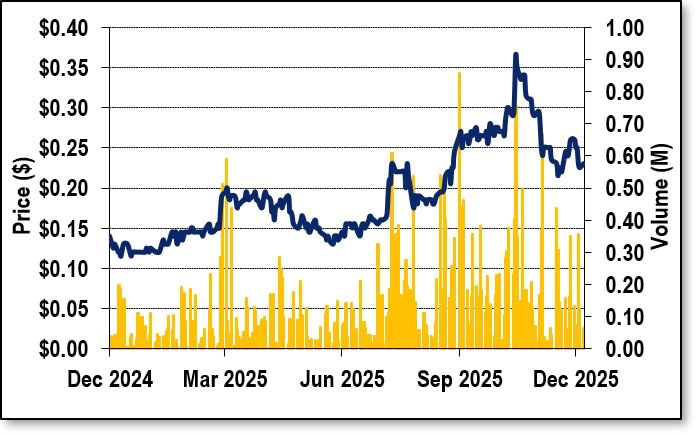

FIGURE 1: One-Year Stock Chart

Other content about SBMI on eResearch.com

- Update Report (December 31, 2024): Strategic Financing Fuels Silver Bullet Mines High-Grade Silver Mine Development in Arizona and Idaho

- Article (December 2, 2024): Developments Bolster Silver Bullet Mines’ Growth Prospects and Revenue Generation Strategy

- Update Report (November 8, 2024): Silver Bullet Mines Battles Challenges to Forge Ahead at the Buckeye Silver Mine & Washington Mine

- Video (February 3, 2022): InvestorIntel Video – Tracy Weslosky Interviews Chris Thompson about eResearch Launching Coverage on Silver Bullet Mines

- Initiation Report (December 7, 2021): Silver Bullet Mines (TSXV: SBMI)

- Video (March 1, 2021): Panel Discussion on Silver with Chris Thompson, Peter Clausi, and Peter Krauth

Notes: All numbers in CAD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.