eResearch is pleased to publish an Update Equity Research Report on DATA Communications Management Corp. (TSX:DCM | OTC: DCMDF).

We are maintaining a Buy rating and a one-year price target of $4.50.

You can download our 18-page Equity Research Report by clicking on the following link: eR-DCM-2023_03_10_UR-M&A-RRD-Can-FINAL2

Company Overview

DCM is a Canadian-based provider of marketing and business communication solutions to companies in North America. Its technology-enabled content and workflow management capabilities solve the complex branding, communications, logistics, and regulatory requirements of leading enterprises, so its customers can accomplish more in less time. Its services include printing, data & content management, labels & asset tracking, location-specific marketing, and multimedia campaign management.

COMPANY UPDATE:

- DCM reported two events recently that were both positive for the Company valuation according to our model.

- On February 22, 2023, DCM announced that it agreed to acquire the Canadian operations of R. Donnelley & Sons Company (RRD) for a cash purchase price of C$123 million.

- The acquisition is expected to close in Q2/2023. It is subject to customary closing conditions and receipt of third-party and regulatory approvals.

- In 2022, RRD Canada generated approximately $250 million in revenue with 10 locations across Canada and 1,000 employees.

- Also, on February 22, DCM reported preliminary full-year financial results for 2022 with revenue in the range of $270 million to $274 million, a 15% to 16.5% increase compared with 2021, Gross Profit in the range of 30.5% to 31%, a 20% to 21% increase compared with 2021, and EBITDA in the range of $35.5 million to $36.5 million.

Figure 1: DCM and RRD Canada – National Reach & Capabilities

Figure 2: DCM and RRD Canada – Pro Forma

FINANCIAL ANALYSIS & VALUATION:

- We adjusted our model under the two scenarios: (1) 2022 annual revenue higher than our estimate and (2) the merger with RRD Canada.

- In Scenario 1, the revenue increase caused our Equal-Weighted Target Price (1 year) to increase to $4.59 from $4.44.

- In Scenario 2, we adjusted our model to reflect the acquisition of RRD Canada and added $250 million in revenue, pro-rated to start in Q4/2023. The acquisition of RRD Canada caused our Equal-Weighted Target Price (1 year) to increase to $5.92 from $4.44.

- The combined impact of the two scenarios caused our Equal-Weighted Target Price (1 year) to increase to $6.02 from $4.44.

However, until the full 2022 financials are released or the merger closes, we are maintaining a Buy rating and a one-year price target of $4.50.

You can download our 18-page Equity Research Report by clicking on the following link: eR-DCM-2023_03_10_UR-M&A-RRD-Can-FINAL2

Other DCM Research Reports:

- Update Report (November 11, 2022): Double-Digit Quarterly Revenue Growth Continues Positive Business Momentum and Strong EBITDA in Q3/2023

- Update Report (August 23, 2022): Strong Business Momentum Continues with Y/Y Revenue Growth of Over 23% in Q2/2022

- Update Report (July 29, 2022): DCM Corporate Strategy Drives Business Transformation with Q1/2022 Producing Largest Revenue Growth in 4 Years

- Update Report (April 29, 2022): DCM’s Quarterly (Q4/2021) Revenue Improves Y/Y as a Sign of COVID Impacts Easing

- Update Report (November 24, 2021): DCM Q3 Financials In-line as Consolidation Improves Cash Flow

- Initiation Report (August 16, 2021): Digital-First Strategy and Tactical Consolidation Drives EBITDA Growth at DCM

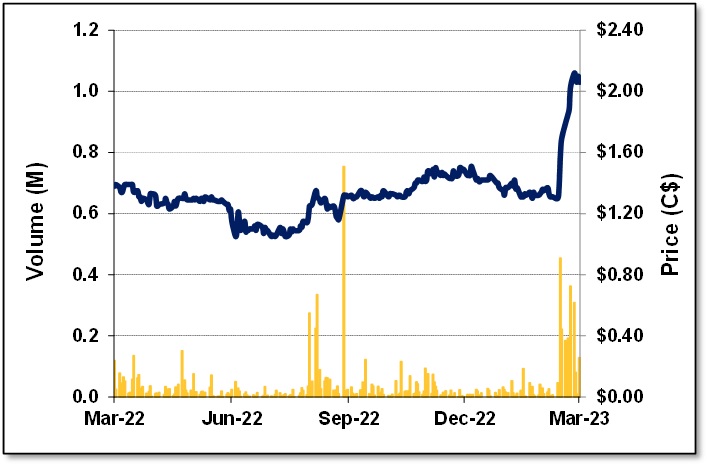

Figure 3: One-Year Stock Chart

Notes: All numbers are in CAD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.