The Technical Program included a series of speakers and panelists to tackle that uncertainty from multiple angles: Mark Cutifani on leadership in volatile times; a panel on whether copper or gold would outperform; a deep dive into lithium’s evolving role; and a discussion on uranium’s return to relevance.

Each session explored value creation not just for investors but also for communities and the environment. The goal wasn’t to crown a winning commodity but to unpack the trends shaping future decisions: electrification, climate policy, emerging technologies, and strategic supply constraints.

The Big Decisions: Leadership in Volatile Times

Vale Base Metals (BOVESPA: VALE3) chairman Mark Cutifani laid out a pragmatic view on leadership in uncertain times. Drawing from his decades in mining, he focused less on theory and more on results.

He opened with research on leadership using companies on the NYSE: “successful” CEOs, those with better stock price performance, made twice as many decisions as their peers. Not all are right, but more decisions mean more progress. “You’ve got to be prepared to fail,” he said, “and to shift direction when the facts change.”

In mining, geology matters. But, so does mining strategy. He tied returns to how well leaders understand both. And optionality, having viable plan Bs, was a recurring theme. He noted that top-performing projects deliver at least 10% free cash flow after replacing resources. That doesn’t happen without deep knowledge of the project, geology, and capital requirements.

In Sudbury at Inco, the Stobie mine turnaround marked one win from prudent capital allocation. They focused on the higher margin mining and de-bottlenecking the other steps. This effort helped lift returns from 7% to 30%. Later, at Anglo American, restructuring dropped the portfolio from 68 to 37 assets but, because of focus, production at the remaining assets went up 40%. And over the next nine years, costs fell 40%. Sometimes, he said, you need to sell your “best” assets to survive.

Cutifani pushed for early community engagement, especially with Indigenous communities. Sustainability, for him, wasn’t a buzzword. It was economics: safety, costs, capital discipline, and social license. Ignore one, and risk the rest.

Technology and geopolitics are harder to forecast. But ignoring them is worse. He pointed to volatile nickel and copper markets as proof. Business periods when capital costs less than market returns are where value gets built.

He circled back to leadership. Decisions don’t land without alignment. “Bring the team with you,” he said. “That’s when the tough calls stick.”

The message wasn’t flashy. It was operational. Leadership is knowing the ore body, managing the margins, and keeping your head when markets don’t.

Copper vs. Gold: Which Metal Will Outperform?

The copper-versus-gold debate brought sharp contrasts. Frank Nikolic from CRU opened with copper’s edge in profitability. Over the last five years, copper companies have delivered better returns than gold producers. The demand case was clear: decarbonization, AI infrastructure, and urban growth. CRU forecasts a 6 to 8 million tonne supply gap in the next decade, needing $100 billion in new capital.

David Strang from Ero Copper (TSX: ERO) backed the call. He projected copper demand hitting 50 million tonnes annually by 2050. He pointed to rising usage in India and Indonesia, likening copper’s spread to the post-war refrigeration boom. The industry, he argued, is in crisis as costs are up, timelines long, and projects scarce. Recycling and brownfield expansions won’t be enough without higher incentive pricing.

Jason Attew from Osisko Gold Royalties (TSX: OR) flipped the argument. Gold’s value, he said, wasn’t industrial. It’s monetary. With US federal debt at $36.5 trillion and interest payments climbing, gold provides insurance. Inflation, geopolitical friction, and the risk of a financial crisis make a stronger case for gold. He questioned copper’s fundamentals if macro conditions deteriorate.

Lawson Winder from Bank of America Securities (NYSE: BAC) added that Central Banks are buying gold at record levels. He emphasized its cultural role and compared it to digital assets like Bitcoin, which he said carry counterparty risks. He also pointed to gold equities offering more diverse strategies for investors.

On the geopolitical front, Gracelin Baskaran of the Center for Strategic and International Studies (CSIS) raised concerns about resource nationalism, especially in the DRC and Indonesia. Strang dismissed it as noise as he thinks economic growth and innovation will matter more. But the rest of the panel saw political risk as real, impacting both gold and copper projects.

The group didn’t land on a clear winner. Instead, the session laid out two distinct value cases. Copper has industrial tailwinds. Gold, macro insurance.

FIGURE 1: Gold vs Copper

Future of Lithium: Trends, Price Pressures, and Emerging Players

Robert Johnston from Columbia University set the stage with the IEA’s forecast: lithium could be the fastest-growing commodity by 2035. But the road ahead isn’t smooth. A large supply gap looms, and emerging tech like Direct Lithium Extraction (DLE) hasn’t scaled yet. He flagged a need for massive investment in battery growth for both Electric Vehicles (EVs) and grid storage.

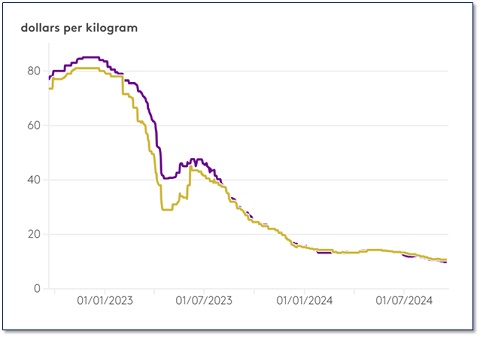

Yasemin Esmen from Fastmarkets offered a pricing snapshot. Battery-grade lithium carbonate peaked at $81/kg in late 2022 but now sits around $9.75/kg in Asia. Lithium hydroxide is close behind at $9.08/kg. Futures trading is gaining ground, especially on the CME. She pointed out demand softness from slower EV growth and high interest rates. But AI-driven data centers and battery storage may fill the gap.

Siddarth Subramani of Hatch focused on near-term supply challenges. Argentina’s ramp-up faces delays tied to permitting, financing, and technical hurdles. He noted the industry was overly bullish on new capacity and too bearish on demand. Recycling and sodium-ion batteries were flagged as future variables but not short-term fixes.

Patrick Howarth from ExxonMobil (NYSE: XOM) “drilled” into Direct Lithium Extraction (DLE). Experts believe it is cleaner than hard rock mining and less water-intensive than lithium mining using traditional brines. The company is betting on the technology, seeing an entry point into the EV and energy storage sectors. Still, DLE currently remains tough to scale and needs more validation before it could be a meaningful supply source.

China’s dominance in the lithium market is hard to ignore. Esmen and Subramani both raised concerns about Beijing’s dominance in refining and technology. The global supply chain could be negatively impacted by any issues around export restrictions, licensing rules, or geopolitical friction. The panel agreed, diversifying lithium sources is a must.

Substitution, recycling, and energy storage all factor into demand. But the signal was clear: without new investment and tech scale-up, the lithium market’s growth could stall just when it’s needed most.

FIGURE 2: Lithium Hydroxide and Lithium Carbonate Prices

Uranium Rebooted

Per Jander of WMC laid out a straightforward case for uranium. He’s spent 20 years in the nuclear fuel business and sees the market finally turning a corner. The fundamentals? Low carbon, high reliability, and geopolitical relevance.

WMC, based in the Netherlands, focuses on nuclear fuel. It advises Sprott, which runs a major physical uranium trust, and NextGen Energy (TSX: NXE), whose uranium is marketed exclusively through WMC. Jander’s not pushing hype. He’s focused on long-term supply chains, from mining to enrichment.

He walked through uranium’s history, starting from a 2-billion-year-old natural reactor in Africa. It’s dense stuff, literally. Splitting uranium atoms releases huge energy. That process powers reactors, which are essentially steam boilers. He compared them to kettles.

The market has been shaped by politics. After WWII, military stockpiling drove supply. Prices fell for decades. The Fukushima disaster in Japan wrecked investor interest. But now, demand is rising again and it’s driven by decarbonization, energy security, and the push for small modular reactors (SMRs). China, the UK, and France are all planning new nuclear reactor builds.

Uranium’s compact energy profile is part of the appeal. One fuel load can run a reactor for over a year. Easy to store the fuel and low transportation needs. And once a plant is built, it runs cheap. Capacity factors are among the highest of any energy source.

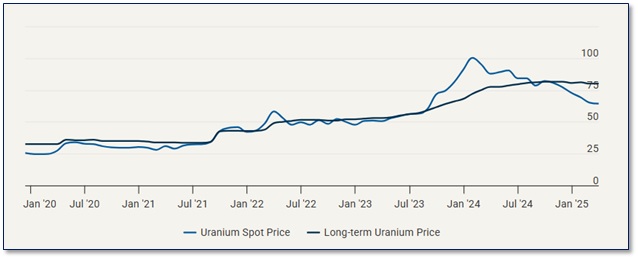

But mining is the pinch point. New projects take 10 to 15 years. Post-Fukushima, few projects advanced, and exploration budgets dried up. That’s starting to change, but not fast enough. Jander showed a long-term supply-demand chart that illustrated stockpiles shrinking and production isn’t keeping pace.

He didn’t overplay the message. The opportunity is there. So are the constraints. Uranium’s path back depends on patient capital, policy support, and a bit of luck. But after years on the sidelines, it’s back in the conversation.

FIGURE 3: Uranium Prices (US$/kg)

Final Thoughts

The discussions underlined a shifting commodity narrative. Copper’s demand story is powerful but faces capital and project bottlenecks. Gold remains a hedge in uncertain times, backed by Central Bank demand and cultural value. Lithium, while volatile, is central to decarbonization and digital infrastructure. Uranium’s quiet comeback is being driven by energy security and long-term power needs.

No single commodity emerged as a clear frontrunner. Instead, the sessions pointed to a more nuanced takeaway: resilience in the resource sector will come from diversification, bold leadership, and smarter capital allocation.

As Doris noted at the outset, what matters most now is how the industry moves from short-term reaction to long-term strategy. That’s where the next big move begins.

Notes: All numbers in CAD unless otherwise stated. The author of this report, as well as employees, consultants, and the family of eResearch, may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice. They do not constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate, and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.