I graduated in Geological Engineering from the University of Toronto in 1959 and joined Dr. Keevil’s company, when gold traded at just US$35 an ounce. At that time, the Keevil Mining Group (KMG) was a loose collection of companies and exploration projects managed by the Keevils, eventually becoming Teck Resources (TSX: TECK.B) by the mid-1970s.

KMG had three gold mines: Pickle Crow, Teck Hughes, and Lamaque. But the only way the mines worked economically was with subsidies. At that time, the Canadian government supported struggling producers through the Emergency Gold Mining Act (EGMA), which added up to $10 per ounce to keep operations running. Of the seventeen gold mines active in Canada at that time, only one did not receive EGMA support.

We stopped exploring for gold and prospected instead for base metals, uranium, and silver.

At the Prospectors Convention (now called the PDAC) in Toronto each year, I would buy a gold sovereign for about $40. Today, all of my ladies now have a necklace with a gold sovereign, a personal connection to a metal that has shaped my life.

Post-Bretton Woods and Inflationary Pressures (1971–1980)

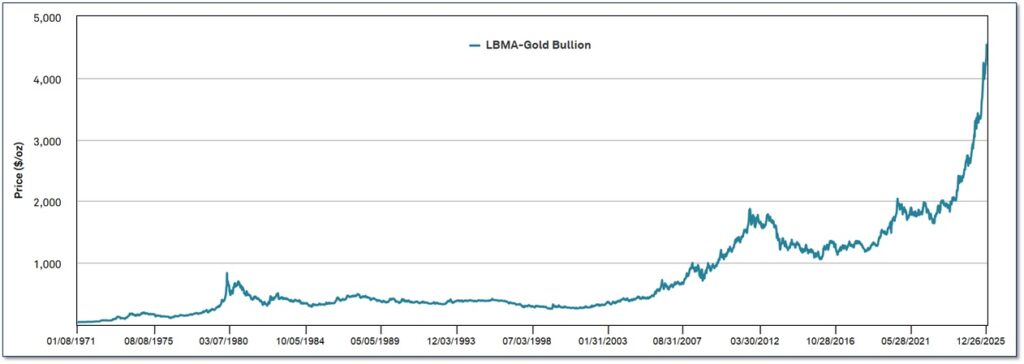

When the Bretton Woods system collapsed in 1971, gold was freed from its peg to the U.S. dollar and began its first true bull market. The price climbed from $35 to $850 per ounce by January 1980.

I was then working with a different company, exploring for gold across Canada, Nevada, and Mexico. We developed several small mines in Nevada and Mexico.

I tried to manage a gold hedging program. It was very difficult for a Canadian living in a safe jurisdiction, as it was usually conditions in some remote part of the world that would move the price of gold. I began to hate that early morning call from our gold trader.

Despite the rising gold price, it was a tough decade for Canadian juniors. Financing was scarce, inflation was high, and investor confidence was fragile. At Lacana Mining, we completed a $7 million financing, one of the few in that period. (Note: Lacana became part of the International Corona in the mid-1980s, which was bought by Homestake Mining in 1992, and eventually became part of Barrick Gold (TSX:ABX) in 2001.)

We started exploring for gold in Nevada with the Cordex syndicate and found a number of small gold mines, including Pinson, Prebble, Dee, and Relief Canyon.

Two moments stand out. First, the Canadian government began selling off the country’s 1,000 tons of gold reserves for a few hundred dollars an ounce, a move that still seems short-sighted. The second was Peter Munk, founder of Barrick Gold, outbidding everyone at $55 million for a Nevada mining property that became Goldstrike, one of the best gold mines ever discovered.

My company, Lacana, was in a Joint Venture with Peter’s junior company and bidding as well. The JV at that time was run by John Livermore. I still have no idea where Peter raised the money or how he determined the bid.

Gold’s rise to $850 was dramatic, but so were the rising costs. Profitability was not what it appeared from the rising gold chart and when Mexico increased its mining taxes, margins shrank even further.

FIGURE 1: A History of Gold Bull Runs and Drivers

Dot-Com Fallout, Financial Crisis, and Commodity Boom-Bust (1980-2012)

In 1986, I joined Anglo American (LSE:AAL), then the world’s largest gold company, to acquire or develop gold projects in North America. We found a few marginal deposits but no breakthroughs. Gold companies were back in favour in the markets and were badly overpriced. When Anglo made a costly acquisition against my advice, I decided it was time to move on.

From 1991 until my retirement in 2017, I was involved with a dozen junior companies, including Golden Queen in California. I stopped trying to predict the gold price as it was a fool’s game. Global events, not geology or logic, seemed to drive the metal’s movements.

Still, the 2000s brought another remarkable cycle. After years of stagnation and decline, gold began to climb again, rising from about $270/oz in 2001 to over $1,900/oz by 2011. This run followed the dot-com collapse, the 9/11 attacks, and the 2008 financial crisis. The rise of gold ETFs made it easier for investors to buy gold. China’s demand for commodities drove a commodity boom across all metals.

I was lucky and made good money on companies I was involved with at the time: Freewest Resources (chromite in Ontario), Chariot Resources (copper in Peru), Consolidated Thompson Lundmark (iron ore in Quebec), and Golden Queen, which were bought out at strong valuations. It was a reminder that opportunities in mining often come from focusing on good projects and ignoring the commodity prices and capital cycles.

Pandemic Response, Trade Tensions, and the Recent Bull Run (2020–2025)

Gold has increased from about US$2,100 an ounce in early 2024 to more than US$4,300 today (and climbing), more than doubling. I have missed the recent fantastic rise in the gold price. Never in my wildest dreams did I envisage gold above US$4,000.

This time, the gold price increase is driven by more fundamental factors, specifically central bank buying. Central banks are diversifying away from the US dollar and are looking to build defences against sanctions and financial risks. These purchases have created a non-speculative demand and a fundamental demand floor for the price of gold.

Institutional investors have joined in as well. With falling real yields in the bond market and high stock market valuations, funds and sovereign investors see gold as a strategic asset and not just an inflation hedge. For technical analysts, the breakout from the long consolidation that started in 2011 has confirmed the shift in upward sentiment.

Compared to the past, the gold price increase we are experiencing now is the result of structural changes in the financial world and a deep revaluation of gold rather than a speculative increase. Central bank purchases because of geopolitical conditions further support this claim.

Final Thoughts

Looking at history, each gold bull market seems to have developed from what the market was dealing with at the time. The 1970s dealt with high inflation, the financial crisis was in the 2000s, and the 2020s have been shaped by geopolitical realignments.

What does not change is gold’s ability to reflect uncertainty in the world. The gold price rises when confidence in paper money weakens. It waits patiently during the good years to remind us that value is sometimes measured in resilience, not returns.

I missed this latest run. About 10 years ago, I began shifting to dividend-paying companies. I was sure the long lead time to build mines was incompatible with my investment time horizon. I still have a few gold positions, but it’s mostly for sentiment.

After sixty-five years in this industry, I don’t try to predict gold’s price, as gold doesn’t change; the world around it does.

Whether this is a long-term trend or a cyclical peak remains to be seen. Gold’s current price and market dynamics suggest it is being reassessed as not only a defensive asset, but a strategic one in the investor’s portfolio.

Good luck to you gold bugs.

FIGURE 2: Gold Price (US$/oz) – 1971 to 2025

Notes: All numbers in CAD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.