Royal Gold Inc. (NASDAQ: RGLD) announced definitive agreements to acquire Sandstorm Gold Ltd. (TSX: SSL | NYSE: SAND) and Horizon Copper Corp. (TSXV: HCU) in deals worth approximately US$3.5 billion and $196 million, respectively.

The deals, which are expected to close in late 2025, will continue to position Royal Gold as one of the largest precious metals streaming and royalty companies in North America with greatly expanded assets and commodity exposure.

The deals are part of a larger trend of consolidation and diversification in the mining royalty space. Investors seek low-risk exposure to gold as precious metals prices rise and other minerals that will benefit from the global transition to clean energy and infrastructure development.

Transaction Terms

Royal Gold will acquire Sandstorm in an all-share deal. Sandstorm shareholders will receive 0.0625 Royal Gold shares for every Sandstorm share, which is a 21% premium to the 20-day volume-weighted average price (VWAP) and a 17% premium to the July 3 closing price. The estimated value of the deal is around US$3.5 billion.

The purchase of Horizon Copper will be an all-cash deal at $2.00 per share, which is an 85% premium to the 20-day VWAP and a 72% premium to the July 4 close, valuing the transaction at around $196 million (approximately US$145 million).

Royal Gold shareholders will own approximately 77% of the combined company, and Sandstorm shareholders approximately 23% (approximately 19 million new Royal Gold shares will be issued).

Standard deal protections are in place, with termination fees set at US$200 million to be paid to Sandstorm or US$130 million to be paid to Royal Gold in some cases.

Portfolio and Operations

The combined company will have 393 streaming and royalty assets, including 80 producing properties and 47 development projects. Production from the expanded portfolio is expected to grow annual gold equivalent ounces by approximately 26% in the first year after the transaction closes. No asset will account for more than 13% of the net asset value.

Royal Gold estimates that 87% of the revenue will come from precious metals (gold accounts for around 75%). Copper and other metals will help diversification.

Key producing mines include Mount Milligan (Canada), Pueblo Viejo (Dominican Republic), Cortez (U.S.), Andacollo (Chile), Khoemacau (Botswana), Wassa (Ghana), and Antamina (Peru). Development-stage assets include MARA (Argentina), Hod Maden (Turkey), and Platreef (South Africa).

Financial and Governance Details

After the deals close, Royal Gold is expected to have a modest closing leverage, with no specific financing sources publicly disclosed. The available credit lines and existing cash flows are likely financial sources to support the deals and continued investment.

In support of the deals, voting support agreements are in place, representing approximately 54% of Horizon shares and 6% of Sandstorm shares. Approval by a two-thirds majority of votes cast by Sandstorm and Horizon shareholders, and minority approval under Canadian securities rules.

Royal Gold will remain headquartered in Denver, Colorado, with Bill Heissenbuttel as President and CEO.

Industry Trends

Due to the global shift towards clean energy, electrification, and infrastructure developments, there is a growing demand for copper, nickel, lithium, and cobalt as these minerals are used in electric vehicles, batteries, and renewable energy technologies. At the same time, gold continues to be an important financial asset and is in the spotlight because of its recent move above US$3,300.

In the streaming and royalty sector, the trend is towards creating diversified, lower-risk portfolios across multiple commodities and jurisdictions. This includes diversifying into base metals such as copper, to capture growth related to electrification and infrastructure investments.

Streaming and royalty financing, which gives miners upfront capital in return for future production at discounted prices, continues to be an attractive non-dilutive source of financing.

Already this year, we have seen several noteworthy deals, including:

- Franco-Nevada (TSX: FNV | NYSE: FNV) announced a US$449 million financing package in January with Discovery Silver (TSX: DSV) on the Porcupine Complex that included a 4.25% net smelter return royalty, a US$100 million senior secured term loan facility, and a US$49 million equity investment.

- Triple Flag (TSX: TFPM) acquired Orogen Royalties (TSXV: OGN) in a $421 million transaction (approximately US$305 million) in April, structured through a mix of cash, shares, and spinout equity. The deal was primarily driven by Orogen’s0% net smelter return (NSR) royalty on AngloGold’s (NYSE: AU) Expanded Silicon gold project in Nevada, also known as the Arthur Gold project.

- Franco-Nevada (TSX: FNV | NYSE: FNV) announced the acquisition of a 7.5% gross margin royalty on the Côté Gold Mine in Ontario for $1.05 billion in May. The mine is operated by IAMGOLD (TSX: IMG) and jointly owned with Sumitomo Metal Mining (TSE: 5713).

- Earlier this month, Eagle Royalties (CSE: ER) announced it had entered into a definitive agreement with Summit Royalty for a reverse takeover (RTO) of Eagle. The resulting entity will hold more than 40 royalty and streaming interests, with a primary focus on precious metals.

For more information on Royalty and Streaming companies, download eResearch’s industry report: Mining Royalty and Streaming Companies: A Low-Risk Path to Mining Exposure

Final Thoughts

Royal Gold’s acquisition of Sandstorm Gold and Horizon Copper aligns with industry trends as it adds scale, geographic diversity, and additional commodity exposure, especially in copper.

This sets the combined company up to benefit from rising gold prices, the transition to battery and battery metals minerals, and to better compete in a changing market environment of increasing capital requirements.

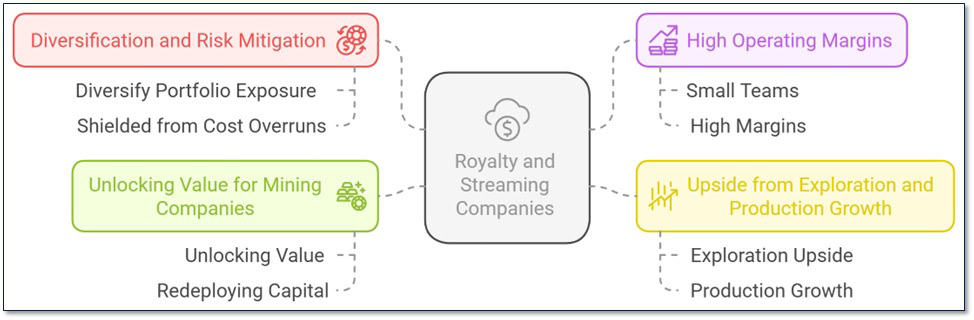

FIGURE 1: Benefits and Strategies of Royalty & Streaming Companies

Notes: All numbers in CAD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.