Canadian Gold Corp (TSXV: CGC | OTC: STRRF | DB: 8S8) (canadiangoldcorp.com) has momentum on its side along with a significant investment from a well-known mining financier. The exploration and project development firm is focused primarily on advancing the past-producing Tartan Lake Gold Mine in Manitoba’s Flin Flon Greenstone Belt.

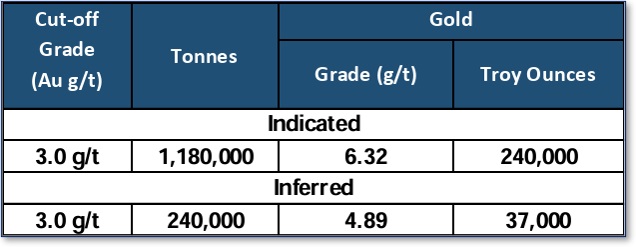

About 47,000 gold ounces were extracted from the Tartan Mine in the late 1980s. An estimate from 2017 shows an Indicated resource of 240,000 ounces of gold for a total resource of 277,000 ounces of gold. The Indicated resource has an average grade of 6.32 grams per tonne (g/t) gold. Notably, the Company has drilled 23,683 metres since 2021, which has extended the resource’s vertical depth by 79%.

CGC plans to expand mineralization in the Main Zone and further explore the South Zone. Drill results over the past four years will be included in a pending updated resource estimate.

Strategic Investment by Rob McEwen and McEwen Mining

The Company also recently closed a C$3 million equity financing. Rob McEwen, former CEO of Goldcorp, subscribed to the offering and now owns 32% of Canadian Gold Corp. And, McEwen’s current firm, McEwen Mining (TSX: MUX), owns an additional 5.9% equity stake in Canadian Gold following the financing.

Most recently, the Company reported that it will use the funds to double the size of its Phase 4 drill program. It will boost Phase 4 drilling to about 8,000 metres. This is in addition to the 23,683 metres drilled since the 2017 resource estimate. And, by targeting high-priority zones with the South and Main zones, the Company expects to expand the resource base significantly.

Also, on April 9, CGC announced it would receive an additional C$300,000 grant from the Manitoba Mineral Development Fund. The grant money is expected to be used for the updated Tartan Mine resource estimate. It will also be directed towards completing a Preliminary Economic Assessment (“PEA”) ahead of a potential mine restart. Both are expected to begin early this summer following the conclusion of its Phase 4 exploration program.

Path to Re-Start Production

CGC is making notable progress on its restart roadmap for the Tartan Mine. The mine benefits from significant infrastructure, including road access and renewable grid power, which could reduce capital intensity.

Importantly, Manitoba’s supportive mining policies, including the New Mines Tax Holiday and access to funding via the Manitoba Mineral Development Fund, contribute to a more favorable permitting environment.

With CEO Michael Swistun’s prior experience in economic development at the provincial level, the Company appears well-positioned to navigate environmental and community approvals.

During a recent presentation, CEO Michael Swistun said he believes the Tartan Mine can be restarted for about C$50 million. Once the Company raises the money, the timeline for commencing underground operations is estimated at two to three years, a relatively short development window in Canada these days. All of these factors lower the project’s permitting risk and enhance its economic appeal.

FIGURE 1: Tartan Lake Mine Resource Estimate

Valuation, Catalysts, and Peer Benchmarking

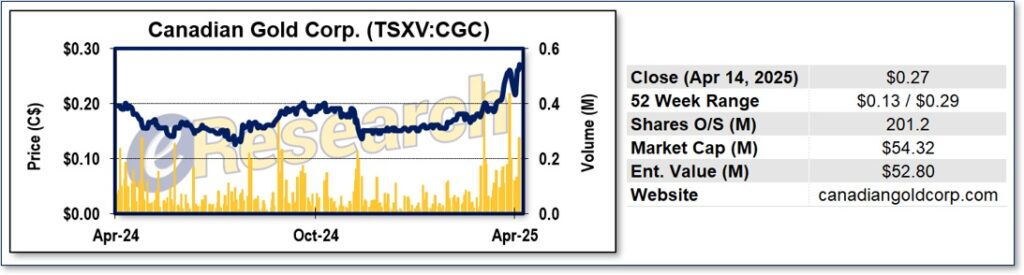

All in all, the Company raised C$4.25 million and has drilled 9,000 metres during the past seven months. Each one of those drill holes contained gold. These corporate developments and exploration execution have helped propel CGC’s stock price about 80% higher year to date. Its stock is currently trading at $0.27 per share.

At an Enterprise Valuation (EV) of approximately $58.3 million, CGC is currently trading at an enterprise value per ounce (EV/oz) of roughly C$210, based on its current resource estimate of 277,000 ounces of gold. This figure is in line with other Canadian exploration-stage companies that have defined mineral resources but are still pre-PEA.

An updated NI 43-101 mineral resource estimate is expected this year and will incorporate over 30,000 metres of additional drilling. If the resource grows meaningfully as anticipated, the EV/oz metric should decline accordingly, improving the company’s relative valuation versus peers.

Several key factors could justify a premium multiple, including (1) the high average grade of 6.32 g/t gold, (2) the presence of existing infrastructure and grid power access, (3) its location in a Tier-1 mining jurisdiction in Manitoba, (4) strategic backing by Rob McEwen and McEwen Mining, and (5) strong near-term resource expansion potential, as demonstrated by multiple high-grade intercepts across the Main, South, and Hanging Wall zones.

CGC also owns two additional exploration-stage projects: Hammond Reef in northwestern Ontario and Malartic South in Quebec. Hammond Reef is located adjacent to the five million plus ounce Hammond Reef gold deposit owned by Agnico Eagle. Surface sampling conducted in 2024 revealed grades as rich as 35.4 g/t gold.

Malartic South, meanwhile, is a 22 square kilometre (km) land holding situated 2.3 km from Agnico Eagle’s Malartic Mine. Canadian Gold Corp says gold mineralization in the northeastern section of the property resembles that of the Malartic Mine.

Final Thoughts

CGC also has multiple near-term catalysts, including the new resource estimate, the launch of a PEA, and ongoing Phase 3 drilling results. Together, these events could significantly enhance the company’s profile and provide further re-rating opportunities.

Canadian Gold Corp completed a strategic transition in 2024 after appointing Michael Swistun as President and CEO. Swistun brings more than 30 years of experience in corporate finance, M&A, and public policy. His previous roles include Director of Acquisitions at Exchange Income Corp and Secretary of Manitoba’s Economic Development Board, where he oversaw major investment initiatives.

Swistun’s dual background in capital markets and government relations could be instrumental as CGC moves into a more advanced development phase. The board now also includes Rob McEwen as the largest shareholder.

With a combination of technical expertise, regulatory experience, and financial stewardship, the current management team is structured to advance the Tartan Mine toward production while positioning the company for potential asset expansion and strategic partnerships.

Rob McEwen and McEwen Mining’s interests in CGC have provided a big boost to its stock price. Additional drill results and an updated resource estimate for the Tartan Mine could provide further catalysts for its shares.

FIGURE 2: CGC 1-Year Stock Chart

Notes: All numbers in CAD unless otherwise stated. The author of this report, employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article. eResearch may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice, nor do they constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate, and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.