Newmont Corporation (NYSE: NEM), the world’s largest gold miner, continued its ambitious divestment program in 2024, aimed at offloading non-core assets to strengthen its balance sheet and return capital to shareholders. The company has already exceeded its $2 billion target for non-core asset sales. It completed a series of high-profile deals across multiple continents, generating up to $3.9 billion in proceeds from a combination of non-core mine sales ($3.4 billion) and investment sales ($527 million).

Following its $19 billion acquisition of Newcrest, Newmont announced in February that its focus on Tier 1 assets and raising $2 billion through the sale of non-core operations. By the company’s definition, Tier 1 assets can generate a minimum of 500,000 ounces of gold equivalent for at least 10 years, while also increasing the company’s copper exposure.

The company intended to divest six non-core assets (Akyem, Cripple Creek & Victor, Éléonore, Musselwhite, Porcupine, and Telfer), as well as two non-core projects (Coffee and Havieron).

Newmont Ringing Up the Asset Sales

In Canada, Newmont has sold two significant operations. UK-based Dhilmar (private) acquired the Éléonore underground gold mine in Quebec for $795 million in cash. This deal is expected to close in the first quarter of 2025 and is a major milestone in Newmont’s divestiture program. Newmont is also selling its Musselwhite mine in Ontario for $850 million to Orla Mining (TSX: OLA), including $810 million in cash, and up to US$ 40 million more contingent on the price of gold over the next two years.

In the US, Newmont agreed to sell its Cripple Creek & Victor (CC&V) Gold Mine in Colorado to SSR Mining (TSX: SSRM) for $275 million. This deal comprises $100 million in cash and two, $87.5 million, deferred payments that are subject to regulatory approvals.

Newmont’s divestment strategy also extended to Africa, with the sale of the Akyem Gold Mine in Ghana to China’s Zijin Mining (SEHK: 2899) for $1 billion. Zijin will pay Newmont $900 million upfront upon closing, with an additional $100 million contingent on Ghana’s Parliament approving mining lease extensions. Akyem is one of Ghana’s largest gold mines and has been producing gold since October 2013 and has significant gold resources and reserves.

In Australia, Newmont sold its 70% ownership in the Havieron project, its Telfer mine, and other related interests in the Paterson region to Greatland Gold (AIM: GGP) for $475 million. This deal includes $207.5 million in cash, $167.5 million in Greatland shares, and a $100 million deferred cash payment linked to gold prices and production from Havieron.

FIGURE 1: Deal Value Summaries (click to enlarge)

Newcrest Deal – Buy Low

According to S&P Capital IQ, the Newcrest deal was consummated at an Enterprise Value (EV) of $19.15 billion. In Newcrest’s annual resources update last year, it had 56.4 million attributable gold ounces of Reserves and we calculated 96.9 million attributable gold equivalent ounces when incorporating the copper, silver, and molybdenum reserves.

Newcrest reported a total of 109.7 million attributable gold ounces of Measured & Indicated Resources (M&I) and 20.6 million attributable gold ounces of Inferred Mineral Resources. When incorporating the copper, silver, and molybdenum resources, Newcrest had almost 250 million attributable gold equivalent ounces.

With these reserve and resource estimates, the EV-to-reserves ratio for the Newmont and Newcrest merger was almost $200/oz of gold equivalent and the EV-to-resources ratio was calculated at less than $80/oz of gold equivalent ounces.

According to research from S&P Capital IQ, the EV-to-reserves ratio for the Newmont and Newcrest merger was significantly lower than the $373/oz of gold equivalent Reserves average for nine comparable mergers, including Barrick’s (TSX: ABX) acquisition of Randgold Resources and the Northern Star’s (ASX: NST) merger with Saracen. The deal was also well below the average of $139/oz when considering the price paid per ounce of attributable gold equivalent resources (including Reserves, M&I, and Inferred Resources).

Asset Deals – Sell High

Newmont‘s acquisition of Newcrest and subsequent asset divestitures demonstrate a prudent strategy of value creation through strategic buying and selling. The company acquired Newcrest at a relatively low EV-to-reserves and EV-to-resources ratios of $198 per gold equivalent ounce of reserves and $77 per gold equivalent ounce of resources, respectively, and this year has executed a series of asset divestitures at considerably higher valuations:

- Akyem Mine: $909 per gold ounce of Reserves,

- Musselwhite: $567 per gold ounce of Reserves,

- Éléonore: $530 per gold ounce of Reserves, and

- CC&V: $212 per gold ounce of Reserves.

These divestments align with Newmont’s strategy to focus on Tier 1 assets with long-term growth potential. CEO Tom Palmer said these transactions are part of Newmont’s journey to create a portfolio of high-quality gold and copper assets that will generate strong free cash flows for decades.

After selling off its non-core assets, Newmont still expects to produce 5.63 million ounces of gold in 2024 and 144,000 tonnes of copper from its core assets.

FIGURE 2: Newmont’s Portfolio Includes More than Half of the World’s Tier 1 Gold Mines (click to enlarge)

Final Thoughts

Newmont’s divestment program in 2024 is reshaping its global portfolio and enabling the company to focus on its most profitable and strategically important assets. By exceeding its divestiture targets, Newmont has strengthened its balance sheet and sharpened its focus on Tier 1 assets.

As the industry evolves, Newmont’s strategic realignment puts it in a great position to remain the leader in the global gold mining space.

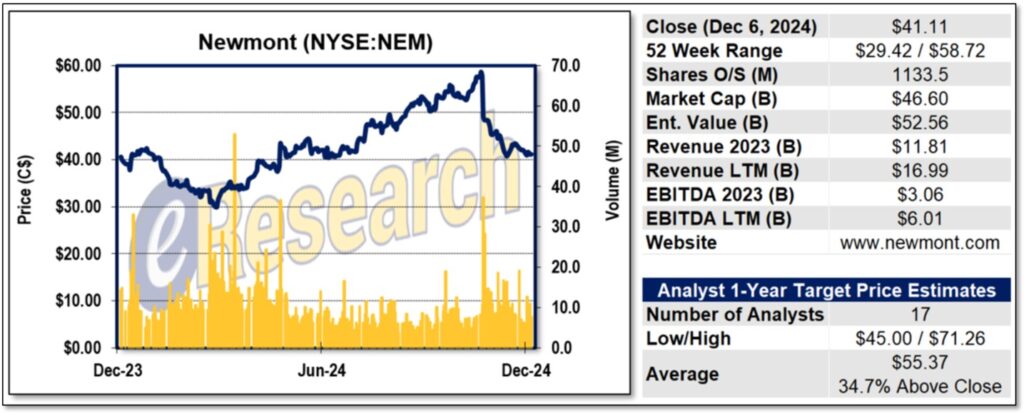

FIGURE 3: Newmont – 1-Year Stock Chart

Notes: All numbers in USD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.