Squarespace Inc. (NYSE: SQSP) has agreed to a privatization transaction with Permira Advisers, a global private equity firm. The deal is structured as an all-cash transaction, valued at approximately $6.99 billion.

Under the deal, Squarespace shareholders will get $44.00 per share in cash. The purchase price represents a 15% premium over its closing price of $38.19 on May 10, and a 29% premium over the 90-day volume-weighted average price before the announcement.

The acquisition is financed through a combination of equity from Permira and debt financing. Key financial institutions involved in providing the debt financing include Ares Capital, Blackstone Credit & Insurance, and Blue Owl Capital. The debt package consists of a $2.1 billion term loan, a $300 million delayed draw loan, and a $250 million revolving credit facility.

The decision was unanimously approved by Squarespace’s board of directors following a recommendation by a special committee composed of independent and disinterested directors.

Valuation Metrics

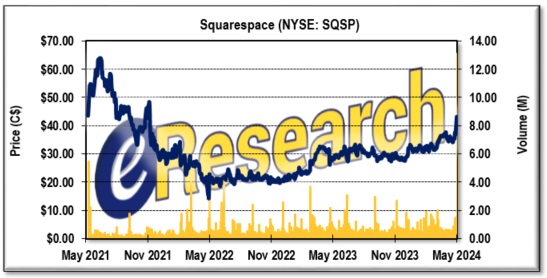

After a direct listing on the NYSE in May 2021 with an opening price of $50 per share, the stock has seen varied performance influenced by broader tech sector trends and its financial results, reaching a high of $64.10 per share in June 2021 and low of $14.44 per share in May 2022 (see Figure 1).

In 2023, Squarespace reported revenue surpassed $1 billion annually, but continued to report Net Losses as it focused on revenue growth and product expansion.

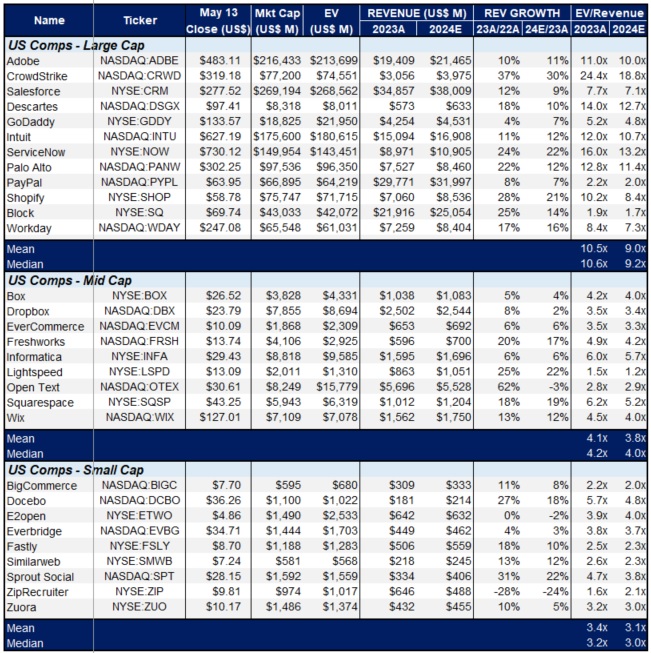

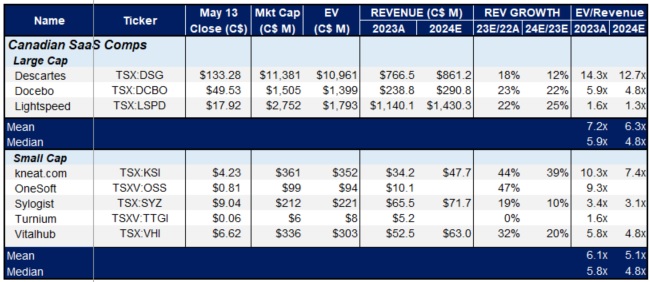

With an Enterprise Value (EV) of $6.99 billion and Trailing Twelve Months (TTM) Revenue and EBITDA at $1.056 billion and $136.0 million, respectively, the deal is valued at 6.6x EV/Revenue and 51.7x EV/EBITDA.

This valuation is at the top end of Comps for US Companies in the Mid Cap space that have an average EV/Revenue in 2023 of 3.8x (see Figure 2).

For 2024, the EV/Revenue estimates for 2024 for each category are:

- US Large Cap SaaS Companies: The average EV/Revenue multiple for 2024 is estimated at approximately 9.0x, with the median at 9.2x.

- US Mid Cap SaaS Companies: The average EV/Revenue multiple for 2024 is estimated at approximately 3.8x, with the median also at 4.0x.

- US Small Cap SaaS Companies: The average EV/Revenue multiple for 2024 is estimated at approximately 3.1x, with the median at 3.0x.

- Canadian Large Cap SaaS Companies: The average EV/Revenue multiple for 2024 is estimated at approximately 6.3x, with the median at 4.8x.

- Canadian Small Cap SaaS Companies: The average EV/Revenue multiple for 2024 is estimated at approximately 5.1x, with the median at 4.8x.

Highest EV/Revenue companies, suggesting growth potential and/or dominant market position include CrowdStrike (NASDAQ: CRWD) at 18.8x, ServiceNow (NYSE: NOW) at 13.2x, and Descartes (TSX: DSG) at 12.7x.

Low EV/Revenue companies, suggesting higher risk and/or higher potential returns include PayPal (NASDAQ: PYPL) at 2.0x, Turnium (TSXV: TTGI) at 1.6x, and Lightspeed (TSX: LSPD) at 1.3x.

About Squarespace

Squarespace is a leading web hosting and website design company known for its design-driven platform which helps companies establish and manage their online presence.

The company offers a wide range of services including website building, domain registration, and e-commerce solutions, empowering users with user-friendly, integrated tools for building and scaling their online operations.

It was founded in 2003 by Anthony Casalena from his college dorm room at the University of Maryland. The company started as a blog-hosting service and expanded into a comprehensive platform supporting a broad array of website creation and management services.

Squarespace’s Major Shareholders Go “All In”

Post-acquisition, Casalena will continue to lead Squarespace as the Chief Executive Officer and will also serve as the Board Chairman. He is rolling in a majority of his existing equity into the deal. Casalena will remain one of the largest shareholders of the privately-held entity.

Major shareholders of Squarespace include General Atlantic and Accel, both of which have been long-term investors in the company. They have also decided to reinvest as part of the go-private deal with Permira.

Figure 1: Squarespace 3-Year Stock Chart

About Permira

Permira is a private, global investment firm that focuses on private equity and venture capital investments across a diverse range of sectors including consumer, healthcare, and technology.

Founded in 1985, Permira has grown to become one of the leading private equity firms in the world, managing funds with a total committed capital of approximately €80 billion as of 2024.

The firm’s major stakeholders include its fund investors, which consist of a mix of institutional investors such as pension funds, sovereign wealth funds, and other private equity firms. Permira’s investment approach is characterized by deep sector knowledge and dedicated industry teams who manage and advise on the investments.

Over the past three years, the firm has been involved in several significant transactions that highlight its strategic focus. Notably, Permira acquired a majority stake in the cybersecurity firm Mimecast in 2021 for $5.5 billion, and participated in the $20.8 billion deal for McAfee in 2021 and the $9.8 billion acquisition of Zendesk in 2022.

Content Management System, e-Commerce, and Web Hosting Ecosystem

Squarespace operates in the website building and web hosting industry, a sector that has seen significant growth due to the increasing demand for digital presence among businesses and individuals.

This industry is characterized by its high dynamism, with continuous innovations in web design, e-commerce solutions, and digital marketing tools to meet evolving user needs.

The industry includes several key players besides Squarespace, each offering unique features or focusing on specific niches:

- Wix.com Ltd. (NASDAQ: WIX): Known for its user-friendly interface and extensive customization options, Wix offers solutions similar to Squarespace but with a stronger emphasis on design flexibility and a broader array of third-party integrations.

- Shopify Inc. (NYSE: SHOP): Specializing in e-commerce, Shopify provides a comprehensive platform for businesses to set up online stores, manage inventory, and process payments. It is particularly popular among retailers looking to expand their online sales.

- WordPress.com: Powered by Automattic, WordPress is highly favored for content management due to its powerful tools and extensive plugin ecosystem. It caters to a range of users from bloggers to large content sites.

- Weebly – acquired by Block, Inc. (NYSE: SQ): Offers a drag-and-drop website builder that is particularly easy to use for beginners. Weebly is often chosen by small businesses and entrepreneurs who prioritize ease of use and simplicity.

- GoDaddy Inc. (NYSE: GDDY) – Although primarily known as a domain registrar, GoDaddy also offers hosting and website-building services. Its marketing tools and domain-focused services make it a one-stop shop for new businesses.

The industry’s growth is driven by the global shift towards online commerce and the increasing need for digital tools that can support remote work, content marketing, and online service management.

Companies in this space compete on various factors including ease of use, customization capabilities, integration options, and price.

As businesses and individuals continue seeking robust online platforms to enhance their digital presence, the demand within this industry is expected to continue growing, spurred by innovations in AI, machine learning, and enhanced e-commerce capabilities.

Figure 2: US and Canadian SaaS Comp Tables

Notes: All numbers in USD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.