eResearch is pleased to publish an update Equity Research Report on Peak Positioning Technologies Inc. (CSE: PKK; OTCQB: PKKFF) pertaining to Peak’s recent release of its Q2/2020 financial statements.

You can download our 15-page Update Report by clicking on the following link: eR-Peak_PKK-UR-2020_09_11_FINAL

//

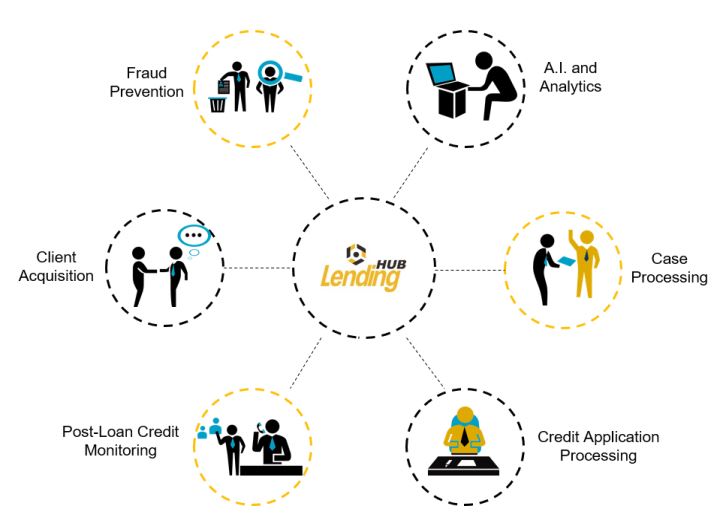

Peak Positioning Technologies Inc. (“Peak” or “the Company”) is the parent company of a group of financial technology (“FinTech”) subsidiaries operating in China’s commercial lending industry. Peak thereby provides an investment vehicle for North American investors looking to participate in China’s FinTech industry.

In China, Peak’s subsidiaries use technology, analytics, and artificial intelligence (“AI”) to provide loans, help small and medium enterprises (“SMEs”) obtain loans, help lenders find clients, and also minimize lending risk. Peak accomplishes this through an ecosystem of lenders, borrowers, loan brokers, and other participants that have come together around its Cubeler Lending Hub platform.

DIAGRAM 1: Peak’s Lending Hub

INVESTMENT HIGHLIGHTS:

- Peak’s revenue in Q2/2020 was $7.3 million compared to $3.9 million in Q1/2020. Revenue for Q2 almost doubled from Q1 and was slightly lower than our estimate of $7.5 million. Peak’s revenue in the quarter continued to benefit from its lending platforms being used to help distribute government relief funds to SMEs that were affected by the coronavirus.

- In Q2/2020, 85% of revenue was generated by Peak’s Fintech Platform. The Company’s FinTech platform’s revenue was $6.2 million compared with $1.1 million from Financial Services. This quarter saw revenue from the Jinxiaoer subsidiary, which we expect to positively impact revenue in H2/2020 and beyond.

- Peak listed shares for trading on the OTCQB stock exchange in the U.S. in July. Peak believes by upgrading the listing to the OTCQB from the OTC Market’s Pink exchange, the Company will gain access to a new pool of U.S. investors. Peak also consolidated shares 1-for-10 and the new share count is reflected in our model and in this report.

- Model Impacts: Due to the lower revenue in Q2/2020, we have slightly increased our Q3 and Q4 revenue estimates to maintain our original 2020 revenue estimate of $35.3 million. We have increased the Outsourcing Services expense thereby reducing EBITDA in 2020 through 2022.

FINANCIAL ANALYSIS & VALUATION:

- We modelled Peak’s revenue for 2020-2022 as a sum of the revenue from the six operating subsidiaries and estimated:

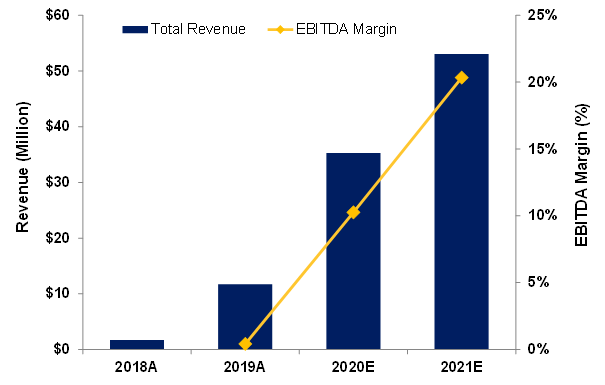

- 2020: Revenue $35.3 million; EBITDA $2.9 million;

- 2021: Revenue $53.1 million; EBITDA $10.8 million;

- 2022: Revenue $58.4 million; EBITDA $15.6 million.

- Using a revenue multiple of 4x 2020 Revenue, an EBITDA multiple of 10x 2020 EBITDA, and a DCF at 10%, we estimate an equal-weighted price per share target of $1.80.

We are maintaining a Buy rating but reducing our one-year price target to $1.80 from $2.00.

//

You can download our 15-page Update Report by clicking on the following link: eR-Peak_PKK-UR-2020_09_11_FINAL

CHART 1: Revenue and EBITDA Margins Actual and Estimates – 2018-2021

Note: All numbers in CAD unless otherwise stated.