eResearch | As businesses become more digital and data driven, cloud products and services are becoming a necessity for all businesses of all sizes to grow and scale, but to support cloud offerings such as Infrastructure as a Service (IaaS) and Platform as a Service (PaaS), large amounts of capital is needed to build the supporting infrastructure.

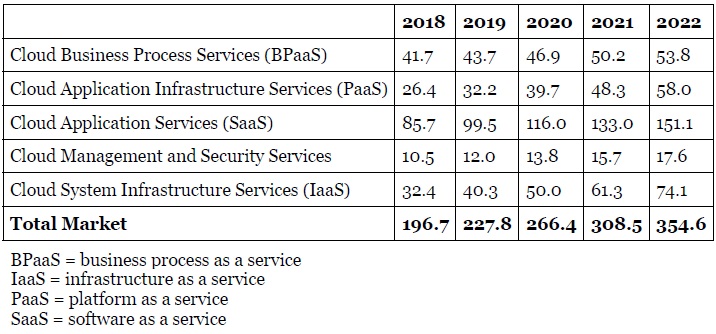

Worldwide Public Cloud Service Revenue Forecast (US$B)

According to Gartner, the cloud infrastructure market is expected to grow 17% to US$266 billion in 2020, with its two main segments SaaS and IaaS forecasted to increase 17% to US$116 billion and 24% to $50 billion, respectively.

Major tech companies such as Alibaba, Amazon, Google, IBM, Microsoft, and Oracle have built vast networks of physical servers to provide these data management services on demand through the internet, supporting online operations, applying data analytics, and securing network connectivity.

North America is currently the leading adopter of cloud computing but in the near future, Asia Pacific demand is expected to outpace North America’s. It will be interesting to see if Alibaba can beat out Amazon and Microsoft once they decide to focus on the western side of the world.

Below are 6 public companies in the cloud race:

Amazon.com, Inc. (NASDAQ: AMZN)

![]()

![]() Amazon leads the cloud race with its Amazon Web Services (“AWS”), the first enterprise grade service for cloud offerings with an online marketplace of 1,500 vendors with over 7,200 service listings.

Amazon leads the cloud race with its Amazon Web Services (“AWS”), the first enterprise grade service for cloud offerings with an online marketplace of 1,500 vendors with over 7,200 service listings.

AWS grew in popularity as it supported 150,000 developers at its launch, and created a gold standard for a simple pay-as-you-go data service that assured developers a secure and efficient data storage and management service.

In Amazon’s most recent Q4/2019 earnings, it generated US$9.9 billion from its cloud business, a 34% increase year-over-year, accounting for 11.6% of its total revenues. Amazon’s growth is attributed to its massive global scaling of datacenters and its focus on winning public cloud service contracts through AWS GovCloud, its isolated datacentre region for government agencies.

Microsoft Corporation (NASDAQ: MSFT)

![]()

![]()

Microsoft’s Microsoft Azure is second in the cloud race as it grew its cloud business rapidly through leveraging its pre-existing ecosystem of services and products (Office, SharePoint, Windows/SQL server, etc.) to seamlessly integrate cloud offerings.

Microsoft is heavily focused on investing in data centers for future contracts and partnerships, such as the US$2 billion cloud contract it won from AT&T. Over 95% of Fortune 500 companies use Microsoft Azure as more companies integrate it into an already existing Microsoft ecosystem.

In Microsoft’s most recent Q2/2020 earnings, it generated US$11.9 billion from its cloud business, a 27% increase year-over-year, accounting for 32% of its total revenues. Growth was mainly due to a 30% increase in its cloud server products and services segment.

Alibaba Group Holding Ltd. (NYSE: BABA)

Alibaba is third in the cloud race as it is the standard cloud infrastructure provider in China and the number one cloud service provider in the Asia-Pacific region, while it currently expands and becomes more localized in Europe.

Though Alibaba may still lack in the breadth of capabilities compared to Amazon Web Services, it is continually expanding features and offerings as its enterprise customers increase spending and become its main growth area.

In Alibaba’s most recent Q2/2020 earnings, it generated US$1.3 billion from its cloud business, a 64% increase year-over-year, accounting for 8% of its total revenues. Growth was mainly due to an increase in spending from enterprise customer.

Alphabet Inc. (NASDAQ:GOOGL)

![]()

![]()

Google’s Google Cloud is starting to make a strong effort to compete with Amazon and Alphabet’s cloud businesses as it caters to developers through supportive open source capabilities and supports organizations who seek reliable AI and machine learning capabilities in cloud offerings.

To compete with Amazon and Microsoft in the cloud race, Google announced a plan last year to triple its cloud sales team while it also built an executive team who had relevant backgrounds at companies such as Microsoft, Oracle, Salesforce, and SAP.

In Google’s most recent Q4/2019 earnings, it generated US$2.6 billion from its cloud business, a 53% increase year-over-year, accounting for 5.7% of its total revenues. This led Google to reach a US$10 billion annual revenue run rate, driven by its cloud infrastructure offerings and its data analytics platform.

International Business Machines Corporation (NYSE: IBM)

![]()

![]() IBM is pivoting away from its core mainframe server business and is focusing on the cloud business through Cloud Pak, which is supported by IBM’s recent $34 billion acquisition of Red Hat Inc. and its cloud SaaS platform.

IBM is pivoting away from its core mainframe server business and is focusing on the cloud business through Cloud Pak, which is supported by IBM’s recent $34 billion acquisition of Red Hat Inc. and its cloud SaaS platform.

IBM and Red Hat can synergize its cloud services by allowing customers to move applications between both cloud platforms seamlessly. IBM now has 2,000 clients for its cloud services, and last quarter, it closed 21 deals worth $10 million each.

In IBM’s most recent Q4/2019 earnings, it generated US$6.8 billion from its cloud business, a 21% increase year-over-year. Success in its cloud business was mainly due to a 19% growth in its Cloud & Data Platforms segment and a 3% increase in its Transaction Processing Platforms segment.

Oracle Corporation (NYSE: ORCL)

![]()

![]() Oracle was slow in the cloud race and is now seen as a niche player in the cloud business as it is focusing on just building infrastructure and renting out data facilities to enterprises, compared with other major players such as Amazon who is providing all types of analytics, security, and data management services.

Oracle was slow in the cloud race and is now seen as a niche player in the cloud business as it is focusing on just building infrastructure and renting out data facilities to enterprises, compared with other major players such as Amazon who is providing all types of analytics, security, and data management services.

To become a larger competitor in the cloud business, Oracle is aggressively expanding its infrastructure as it recently announced the expansion of its data centers to five regions, with offerings now available in 21 locations.

In Oracle’s most recent Q2/2020 earnings, it generated US$7.9 billion for its cloud business, a 1% increase year-over-year, accounting for 83% of its total revenues. Oracle’s lack of cloud business growth is mainly due to its cloud licensing segment, which declined 7% year-over-year, while cloud services and license support grew revenue by 3%.

//

| Company | Cloud Segment | Products & Services | Revenue 2019 (US$) | Annual Growth |

| Alibaba | Alibaba Cloud | Compute Content Delivery Blockchain Database Data analytics Developer Services Domain & Website Elastic Computing Identity Management Intelligent Services IoT Media Services Message Queue Micro Services Network Private Cloud Search and Analytics Storage Security Visualization | $3.7 billion | 64% |

| Amazon | Amazon Web Services (AWS) | Business Applications Compute Customer Engagement Database Developer Tools End User Computing Game Tech IoT Machine Learning Management & Governance Media Services Migration & Transfer Mobile Networking & Content Delivery Quantum Technologies Robotics Satellite Security Storage | $35 billion | 37% |

| Google Cloud | Google Cloud Platform AI and Machine Learning API Management Compute Containers Data Analytics Databases Developer Tools Healthcare and Life Sciences Hybrid and Multi-cloud IoT Management Tools Media and Gaming Migration Networking Security Serverless Computing Storage | $8.9 billion | 53% | |

| IBM | IBM Cloud | Analytics Artificial Intelligence Blockchain Compute Databases Developer tools IBM Cloud Paks Integration IoT Management Migration Mobile Private cloud Network Security Storage VMware | $21.1 billion | 11% |

| Microsoft | Intelligent Cloud | Server Product and Cloud Services Microsoft Azure Microsoft SQL Server Windows Server Visual Studio Systems Center GitHubEnterprise Services Premier Support Services Microsoft Consulting Services | $38.9 billion | 21% |

| Oracle | Generation 2 Cloud Infrastructure | Generation 2 Cloud Infrastructure Application Development Analytics Autonomous Database Compute Cloud Customer Infrastructure Market PlaceCloud Applications Enterprise resource planning Human Capital Management Supply Chain Management Sales Services Marketing Data Cloud NetSuite Application Suite All Cloud Applications | $9.3 billion | 3% |