eResearch is pleased to publish an Update Report on Turnium Technology Group Inc. (TSXV: TTGI | FSE: E48).

We are maintaining a Speculative Buy rating and increasing the one-year price target to $0.35.

You can download our 22-page Equity Research Update Report that covers an in-depth analysis of the company, an overview of recent financials, and our valuation methodology by clicking on the following link: eR-Turnium-2026_05_25_UR-FINAL

Company Overview

Turnium Technology Group Inc. (“TTGI”) is a Vancouver-based public company that delivers scalable, secure, and cost-effective network and Information Technology (IT) solutions through a unified Technology-as-a-Service (TaaS) model.

TTGI operates globally through its three wholly owned subsidiaries: Turnium Network Solutions Inc. (TNSI), Claratti Pty. Ltd. (Claratti), and Insentra, which together form a complete suite of business technology solutions.

- TNSI’s Software-Defined Wide Area Network (SD-WAN) platform enables service providers, IT resellers, and enterprise customers to build and manage secure, resilient wide area networks.

- Claratti delivers telecom, managed networks & IT services, mobile services, cybersecurity, and cloud infrastructure solutions.

- Insentra provides channel-only advisory, professional services, and managed IT solutions across the United States, the United Kingdom, and Asia-Pacific.

Report Highlights

- FQ2/2026 Results in Line:

- TTGI reported revenue of $6.44 million, in line with our estimate of $6.40 million, representing the first full quarter consolidating TNSI, Claratti, and Insentra.

- EBITDA loss was $1.85M, including $0.47M in one-time M&A and financing transaction costs that are not expected in FQ3/2026.

- Guidance Reaffirmed, Sequential Revenue Growth Expected:

- Management reaffirmed revenue guidance of $7.0 million to $7.5 million in FQ3/2026 and $8.0 million to $8.5 million in FQ4/2026, implying continued sequential growth toward the $28 million to $32 million 12-month target.

- A cost optimization program targeting $1.2 million to $2.4 million in annualized SG&A reductions has been initiated to help improve cash flow.

- Insentra U.S. Enterprise Pipeline Building:

- Post-quarter, Insentra secured two six-figure U.S. enterprise contracts, both structured as multi-phase programs with recurring revenue potential.

- These wins validate Insentra’s enterprise credentials and channel-led growth model beyond its core Australian market.

- Balance Sheet Repair Remains a Key Risk:

- Total debt increased to $19.9 million, but includes approximately $7 million in VTB loan & earn-outs.

- The $6.0 million private placement announced March 31, 2026, targets $2.5 million in debt retirement and $3.5 million in working capital.

Investment Thesis

TTGI represents a turnaround opportunity built on three strategic pillars:

- Portfolio transformation from a single-product SD-WAN vendor to a multi-service global TaaS platform.

- Geographic and capability diversification across North America, the UK, and Asia-Pacific with 280+ channel partners.

- Operational leverage, as the $30 million revenue midpoint generates $12.4 million in gross profit, 185% more than FY2025’s $4.35 million, combined with a $1.2 million to $2.4 million annualized cost optimization program.

The Insentra acquisition remains the central pillar of the investment thesis. FQ2/2026 delivered revenue of $6.44 million, in line with our estimate, providing initial validation of the revenue thesis.

Insentra’s strictly channel-only operating model eliminates channel conflict and creates a low-friction environment for cross-selling. Its Microsoft ecosystem expertise, spanning Copilot, Azure AI, and security platforms, is generating tangible enterprise wins, with two U.S. six-figure engagements announced post-quarter in energy services and advanced manufacturing.

The path to positive EBITDA depends on three factors: retention and growth of Insentra’s revenue base; realization of the $1.2 million to $2.4 million annualized cost optimization program; and resolution of the debt and liquidity position, with the announced $6.0 million private placement targeting $2.5 million in debt retirement and $3.5 million in working capital.

Financial Analysis and Valuation

We valued TTGI using an equal-weighted average of DCF and EV/Revenue, which we believe reflects its high recurring revenue mix, margins, and revenue growth profile (organic, improving SD-WAN business, a full-year contribution from Claratti, and Insentra starting FQ2/2026).

We are maintaining our Speculative Buy rating and increasing our 12-month Target Price to $0.35 per share.

You can download our 22-page Equity Research Update Report by clicking on the following link: eR-Turnium-2026_05_25_UR-FINAL

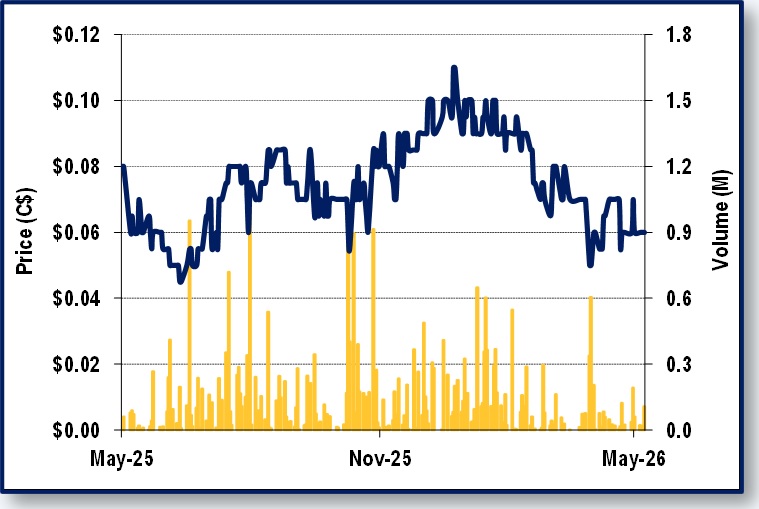

FIGURE 1: 1-Year Stock Chart

Notes: The author, employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article, report, and/or video, and may have been paid by a company mentioned. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Content on eresearch.com is provided for general informational purposes only and does not constitute financial, investment, tax, legal, or accounting advice, nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate, and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.

FQ2/2026 Results in Line:

TTGI reported revenue of $6.44 million, in line with our estimate of $6.40 million, representing the first full quarter consolidating TNSI, Claratti, and Insentra.

EBITDA loss was $1.85M, including $0.47M in one-time M&A and financing transaction costs that are not expected in FQ3/2026.

Guidance Reaffirmed, Sequential Revenue Growth Expected:

Management reaffirmed revenue guidance of $7.0 million to $7.5 million in FQ3/2026 and $8.0 million to $8.5 million in FQ4/2026, implying continued sequential growth toward the $28 million to $32 million 12-month target.

A cost optimization program targeting $1.2 million to $2.4 million in annualized SG&A reductions has been initiated to help improve cash flow.

Insentra U.S. Enterprise Pipeline Building:

Post-quarter, Insentra secured two six-figure U.S. enterprise contracts, both structured as multi-phase programs with recurring revenue potential.

These wins validate Insentra’s enterprise credentials and channel-led growth model beyond its core Australian market.

Balance Sheet Repair Remains a Key Risk:

Total debt increased to $19.9 million, but includes approximately $7 million in VTB loan & earn-outs.

The $6.0 million private placement announced March 31, 2026, targets $2.5 million in debt retirement and $3.5 million in working capital.

Investment Thesis

TTGI represents a turnaround opportunity built on three strategic pillars:

Portfolio transformation from a single-product SD-WAN vendor to a multi-service global TaaS platform.

Geographic and capability diversification across North America, the UK, and Asia-Pacific with 280+ channel partners.

Operational leverage, as the $30 million revenue midpoint generates $12.4 million in gross profit, 185% more than FY2025’s $4.35 million, combined with a $1.2 million to $2.4 million annualized cost optimization program.