eResearch is pleased to publish a New Update Report on Silver Bullet Mines Corp. (TSXV: SBMI) | (OTCQB: SBMCF).

We are maintaining our Speculative Buy rating and increasing our one-year price target to $0.70.

You can download our 17-page Equity Research Report that covers an in-depth analysis of the company and its projects by clicking on the following link: eResearch-SBMI-UR-2026_02_25_FINAL

Company Overview:

SBMI is a precious metals company focused on developing and operating mining assets in the United States. The Company owns and operates a fully permitted mill in Globe, Arizona, and is advancing multiple mining properties, including the King Tut and Super Champ mines in Arizona and the Washington Mine in Idaho.

SBMI is a precious metals company focused on developing and operating mining assets in the United States. The Company owns and operates a fully permitted mill in Globe, Arizona, and is advancing multiple mining properties, including the King Tut and Super Champ mines in Arizona and the Washington Mine in Idaho.

SBMI is pursuing a dual-channel revenue strategy that includes internal processing at its Arizona facility, alongside direct shipping ore (DSO),with additional bulk sample production planned from its Washington Mine in Idaho. The Company’s strategy is centered on transitioning from development stage activities to sustainable cash generating operations through disciplined production growth and asset utilization.

Report Highlights:

- SBMI is advancing a dual revenue model combining Arizona mill concentrate operations and a direct ship ore agreement covering its Arizona assets, and a bulk sample planned from its Washington Mine in Idaho.

- Initial production and sales have validated the full mining-to-payment cycle.

- Projected 12-month revenue of approximately US$15.2 million supports estimated operating cash flow of C$16.1 million.

- The balance sheet has improved following debt conversions, with net cash projected at the end of the 12-month forward period.

- A discounted 7.0x multiple to projected sustainable run rate cash flow yields a 12-month equity valuation of approximately C$135 million, or $0.70 per share on a fully diluted basis.

- Key risks include grade variability, cost control, and the availability of sufficient accessible mineralized material as surface stockpiles are depleted and underground development advances.

Investment Thesis:

- SBMI is transitioning from development stage activities toward small-scale production and cash generation. The Company’s Arizona mill provides infrastructure leverage, enabling both internal ore processing and third-party tolling opportunities.

- Concurrently, DSO offers a lower capital intensity revenue channel. This dual approach reduces reliance on any single asset and provides operational flexibility.

- We treat projected 12-month cash flow as a proxy for sustainable run rate production, assuming continuity of grade and access to mineralized material. The investment case rests on the Company’s ability to demonstrate repeatable mining to payment cycles, maintain stable recoveries, and control operating costs during ramp-up.

- While no NI 43-101 compliant resource has been published for certain properties, operational progress and recent shipments indicate potential for continued production.

- If management executes consistently over the next year, the Company may further de-risk its asset base and strengthen balance sheet flexibility. However, valuation remains sensitive to grade consistency and resource accessibility, cost structure, and production consistency.

Financial Analysis & Valuation:

- Our valuation is based on a projected 12-month operating cash flow of approximately $16.1 million. EBITDA is used as a proxy for operating cash flow before working capital changes.

- We apply a 7.0x multiple to projected sustainable run-rate cash flow, representing a significant discount to peer averages, which show a mean EV/EBITDA of approximately 26.0x and a median of 20.1x. Public market multiples vary widely depending on production stage, with many small producers trading at elevated multiples during ramp-up. We discount the multiple to 7.0x to reflect SBMI’s smaller scale and early production profile.

- After incorporating projected net cash at the forward valuation date and adjusting for full dilution, we derive an equity value of approximately $135 million, or $0.70 per share.

- This valuation assumes stable recoveries, no significant cost escalation during ramp-up, and continued access to mineralized material.

We are maintaining our Speculative Buy rating and increasing our one-year price target to $0.70.

You can download our 17-page Equity Research Report that covers an in-depth analysis of the company and its projects by clicking on the following link: eResearch-SBMI-UR-2026_02_25_FINAL

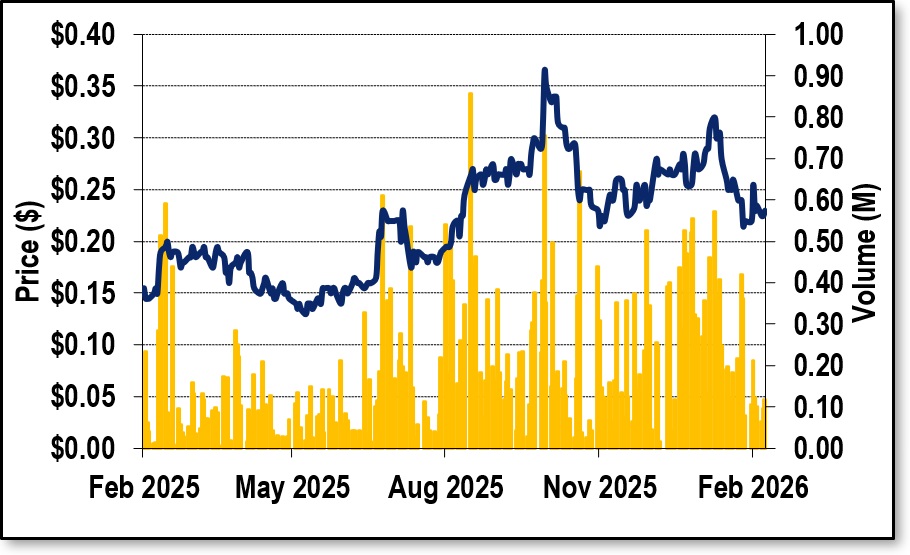

FIGURE 1: 1-Year Stock Chart

Notes: The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice, nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate, and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.