On August 28, 2025, Desjardins Group announced a definitive agreement to acquire Guardian Capital Group in an all-cash transaction valuing the company at approximately $1.67 billion.

The Montreal-based cooperative had already purchased Guardian’s Worldsource businesses back in November 2022. That deal closed in March 2023 for $750 million.

Desjardins is now taking the rest of the company private. When you put both organizations together, you get a combined firm managing roughly $280 billion in client assets.

Deal Terms and Premium

Desjardins is paying $68.00 per share. That represents a 66% premium over where the Class A shares closed on August 27, 2025, and a 48% premium on the common shares.

Looking at the 30-day volume-weighted average, the premiums come in at 65% and 54%, respectively. No financing condition attached to this agreement, just straight cash.

Both boards unanimously approved the transaction. Major shareholders and all directors and executive officers, collectively holding over 32% of Guardian‘s outstanding shares, entered into support and voting agreements.

Some of these shareholders also signed equity rollover agreements, meaning they’ll receive shares in Desjardins Global Asset Management instead of cash.

Looking at the valuation metrics, the deal implies an Equity Value to Net Income multiple of over 11.1x, which is a solid clip, but the real eye-opener is the Price to Forward EPS at almost 45.2x. That’s a lot of growth being baked into the price right out of the gate. The Implied Equity Value to Book Value sits at 1.26x, which is in line with recent transactions in the 1.0x to 2.0x range, including National Bank of Canada acquiring Canadian Western Bank at 1.33x and BMO acquiring Burgundy Asset Management at 1.34x.

From these metrics, it’s a bit of a mixed bag. Desjardins is paying a premium for future growth, but on paper, the current assets look relatively cheap. It makes the whole “strategic leap” thing feel a bit more calculated, even if the forward-looking price tag is enough to give an analyst some pause.

Leadership and Strategic Rationale

George Mavroudis, Guardian‘s current president and CEO, will lead the combined asset management business. He’s been with Guardian since 2005 and took over as president in 2011. Nicolas Richard, president and COO of Desjardins Global Asset Management, will join the executive team.

Guy Cormier, president and CEO of Desjardins Group, positioned the acquisition as a way to strengthen their position in asset management both domestically and internationally. Founded in 1962, Guardian has been a public company for over 60 years. The company managed $164.1 billion in client assets as of June 30, 2025, plus a proprietary investment portfolio worth $1.25 billion.

The strategic thinking here is about scale. Desjardins currently manages about $112 billion, mostly concentrated in Quebec. Guardian brings strength in the rest of Canada, plus international operations in the U.S., U.K., and elsewhere. Together, they can spread the fixed costs of technology, compliance, and regulation across a larger base.

Transaction Timeline and Approvals

The deal requires several key approvals, including a shareholder vote, and normal court and regulatory approvals.

The transaction is expected to close in the first half of 2026. Once it closes, Guardian will delist from the Toronto Stock Exchange.

Recent Acquisition Activity

Desjardins has been active on the M&A front. The November 2022 announcement (closed March 2023) covered three Worldsource entities:

- IDC Worldsource Insurance Network Inc. (Canada’s leading life and health insurance MGA)

- Worldsource Financial Management Inc. (a mutual fund dealer)

- Worldsource Securities Inc. (an independent full-service securities dealer)

These three companies serve over 5,000 advisors across Canada. The deal gave Desjardins more than $2 billion in life insurance premiums in force and added $43 billion in combined assets under administration.

That 2023 acquisition let Guardian focus on its core asset management operations. Now with this second deal, Desjardins is consolidating the entire Guardian platform. Makes you wonder if they had this full acquisition in mind all along or if the relationship from that first deal just made the second one make more sense.

Company Backgrounds

Desjardins Group is the largest cooperative financial group in North America and the sixth largest globally, with assets of $501.3 billion as of June 30, 2025. They’re celebrating their 125th anniversary in 2025. Over 57,200 employees. Forbes recognized them as one of the World’s Best Banks in 2025.

Guardian was founded in Toronto in 1962 as Guardian Management Ltd. The company went public and became one of the first investment counseling firms in Canada to trade publicly.

Over six decades, they built a reputation for steady growth and long-term client relationships. Their investment management business operates through Guardian Capital LP (the successor to the original 1962 business), plus subsidiaries GuardCap Asset Management Limited (London-based, acquired in 2012) and Alta Capital Management LLC (U.S.-based, majority interest acquired in 2017).

Market Context

The market is seeing more of these take-private transactions in the asset management space. Firms realize they need scale to survive as the technology investments, regulatory compliance costs, and competitive pressures keep mounting.

Guardian had been building out internationally but was still relatively small compared to the global players. Desjardins gets instant scale and geographic diversification. Guardian shareholders get paid a decent premium and walk away.

The real test will be integration. Combining two organizations with different cultures, systems, and investment approaches. Desjardins has kept other acquisitions like Worldsource operating as standalone entities, so maybe they’ll take a similar approach here. Keep Guardian‘s investment teams in place, maintain their processes, and just provide the capital and infrastructure support.

Whether the deal delivers long-term value for Desjardins members and clients, we’ll have to wait and see how the integration plays out over the next few years.

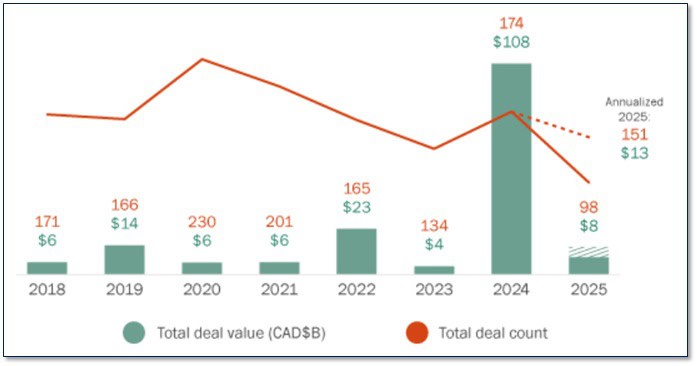

FIGURE 1: Canadian Financial Services Transactions by Deal Value and Volume

Notes: All numbers in CAD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.