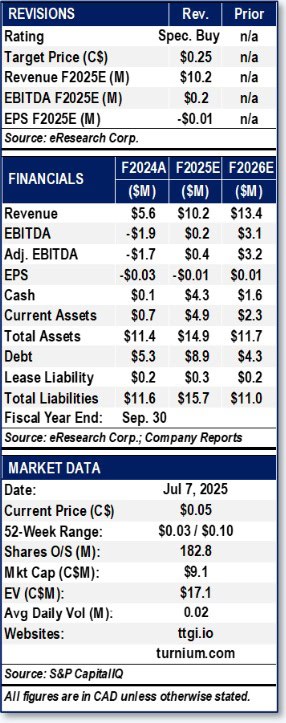

eResearch is pleased to publish an Initiation Report on Turnium Technology Group Inc. (TSXV: TTGI | FSE: E48).

We are Initiating Coverage with a Speculative Buy rating and one-year price target of $0.25.

You can download our 61-page Equity Research Report that covers an in-depth analysis of the company and a detailed overview of its products, by clicking on the following link: eR-Turnium-2025_07_07_IR-FINAL

Company Overview:

TTGI is a Canada-based public company that delivers scalable, secure, and cost-effective network and Information Technology (IT) solutions through a unified Technology-as-a-Service (TaaS) model.

Headquartered in Vancouver, TTGI operates globally through its three wholly owned subsidiaries: Turnium Network Solutions Inc. (TNSI), Claratti, and Tenacious Networks (TNET), each offering complementary capabilities that together form a complete suite of software-defined networking and managed IT services.

- TNSI’s Software-Defined Wide Area Network (SD-WAN) platform enables service providers, IT resellers, and enterprise customers to build and manage secure, resilient wide area networks.

- Claratti delivers managed IT services, cybersecurity, and cloud infrastructure services.

- TNET provides managed IT services, professional services, and value-added resell services.

Report Highlights:

Claratti Acquisition Doubles Revenue Base and Expands the Company Globally

Claratti Acquisition Doubles Revenue Base and Expands the Company Globally- Post-merger, TTGI is positioned to scale recurring revenue and expand globally via its TaaS service model, which caters to any-sized business in the Small and Medium-sized Enterprise (SME) market.

- Platform-Based Growth in Cybersecurity and AI Technology

- TTGI delivers an integrated cybersecurity stack via its TaaS platform, enabling SMEs to adopt enterprise-grade, AI-driven security supported by its global NOC, SOC, and IT Help Desk, aligned with key security compliance standards.

- Expanding Partner Network Through White-Label TaaS

- TTGI enables ISPs and MSPs to brand and deploy its TaaS solution, including its secure SD-WAN services, boosting partner stickiness, upsell, and reach.

- Recurring Revenue Model Drives Operational Leverage

- TTGI’s multi-year SME contracts drive high-margin recurring revenue, providing revenue stability, mitigating market compression and tariffs, and supporting scalable growth and margin recovery.

Investment Thesis:

These competitive advantages position TTGI uniquely in the market and allow it to differentiate itself from other participants.

1) Compelling Relative Valuation

- Currently trading at 1.7x EV/F2025E Revenue, TTGI trades below peer averages (see Appendix B). Our target price of $0.25 implies a 5x upside.

2) Experienced Post-Merger Leadership

- Claratti’s CEO now leads TTGI, backed by a strengthened management team and expanded board with global IT expertise.

3) Technology-as-a-Service (TaaS) Platform Purpose-Built for SME Channel Delivery

- TTGI’s platform has evolved beyond SD-WAN into a fully integrated, subscription-based Technology-as-a-Service (TaaS) offering. Built for its channel partners, the platform targets Small and Medium-sized Enterprises (SMEs) in the 20 to 250-seat range, a segment underserved by larger enterprise IT vendors (see Figure 1).

- TTGI’s TaaS stack combines proprietary SD-WAN with third-party software from Microsoft (NASDAQ: MSFT), Kaseya, Commvault (NASDAQ: CVLT), Fortinet (NASDAQ: FTNT), Forcepoint, and others, enabling delivery of connectivity, security, monitoring, and endpoint management through a single pane of glass.

- The platform supports recurring revenue generation by automating infrastructure visibility, remediation workflows, and sales quote generation for end customers. This approach positions TTGI as the foundational infrastructure (“plumbing”) and secure perimeter (“IT fortress”) supporting SME digital operations.

4) Diversified IT Solutions Platform

- TTGI offers SD-WAN, TaaS, and managed IT services through three business units, delivering complete, cost-effective, scalable IT infrastructure. Claratti’s managed cybersecurity service suite provides the tools for partners to help SMEs comply with various cybersecurity standards (ISO27001, NIST Cybersecurity, Essential Eight) and gain access to its 24×7 Security Operations Centre (SOC), which operates at Level 2 Type II standards.

5) High-Visibility Recurring Revenue Model

- 80% of TTGI’s blended revenue is recurring, with long-term contracts across TTGI’s SD-WAN and Claratti’s TaaS platform providing predictable cash flow.

6) Exposure to High-Growth Markets

- TTGI’s extensive TaaS business model, which incorporates SD-WAN and cybersecurity, is expected to grow at a double-digit annual rate through 2030, based on global IT service trends.

7) Claratti Acquisition Doubles Revenue

- The acquisition of Claratti added scale, recurring revenue, OEM access, and an established customer base in Asia-Pacific.

8) White-Label Platform Drives Stickiness

- TTGI’s fully brandable platform boosts partner loyalty by embedding its TaaS solution and proprietary SD-WAN software into MSP and OEM workflows.

9) Global Reach Through Channel Strategy

- TTGI sells via ISPs, MSPs, and OEMs, expanding its footprint efficiently across North America, Europe, and Asia-Pacific.

10) Cross-Selling and Cost Synergies

- Post-acquisition integration offers cross-selling upside and shared services savings across Claratti, TNSI, and TNET.

11) Margin Expansion Potential

- With software-driven revenue growth and cost optimization, TTGI is targeting gross margins of 75% to 80% in the long term. During FH1/2025, gross margin for the period was 63% compared with 71% in FH1/2024.

12) Flexible, Cloud-Native Architecture

- TTGI’s platform is hardware-agnostic, multi-cloud capable, and supports next-gen devices with AI-based traffic control.

13) Strategic Optionality for Growth or Exit

- TTGI’s platform offers M&A upside, either as a target for larger players or a consolidator of adjacent IT assets.

Financial Analysis & Valuation:

TTGI currently trades at 1.7x EV/F2025E revenue, which is below peer averages.

Our 12-month target price of $0.25 is based on an equal-weighted blend of three valuation approaches: EV/Revenue multiple, EV/EBITDA multiple, and DCF. We believe this method best reflects its current revenue growth profile (both organic and a full-year contribution from Claratti), high recurring revenue mix, and margin profile.

We are Initiating Coverage with a Speculative Buy rating and one-year price target of $0.25.

You can download our 61-page Equity Research Report that covers an in-depth analysis of the company and a detailed overview of its products, by clicking on the following link: eR-Turnium-2025_07_07_IR-FINAL

FIGURE 1: 1-Year Stock Chart

Other eResearch articles on TTGI:

- Turnium Unveils Next-Generation Universal Edge Device Leveraging AI and Post Quantum Cryptography

- Squarespace’s $6.99B Deal Signals Strong Outlook for SaaS Sector

- MediaValet Acquisition Highlights Valuation Trends in Canadian SaaS and DAM Sectors

Notes: All numbers in CAD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor.

The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.