Activist investor Elliott Investment Management has written a letter to Honeywell International (NYSE: HON) asking it to divide into two distinct businesses after recently making a more than $5 billion investment.

Following the pattern of other big industrial corporations choosing to spin off divisions in recent years, Elliott believes that Honeywell Aerospace and Honeywell Automation could benefit from being independent.

The two companies would gain from simpler strategies, focused management, better use of capital, stronger performance, improved oversight, and many other benefits that large companies enjoy after leaving a conglomerate structure.

Elliott noted that Honeywell could do better with a simpler structure, like the changes made by other large companies such as General Electric (NYSE: GE) and United Technologies, now RTX Corporation (NYSE: RTX).

Steinberg and Cohn wrote, “We see clear reasons for these challenges and an easy way to solve them. The conglomerate structure that used to work for Honeywell does not fit anymore, and now is the time to simplify.”

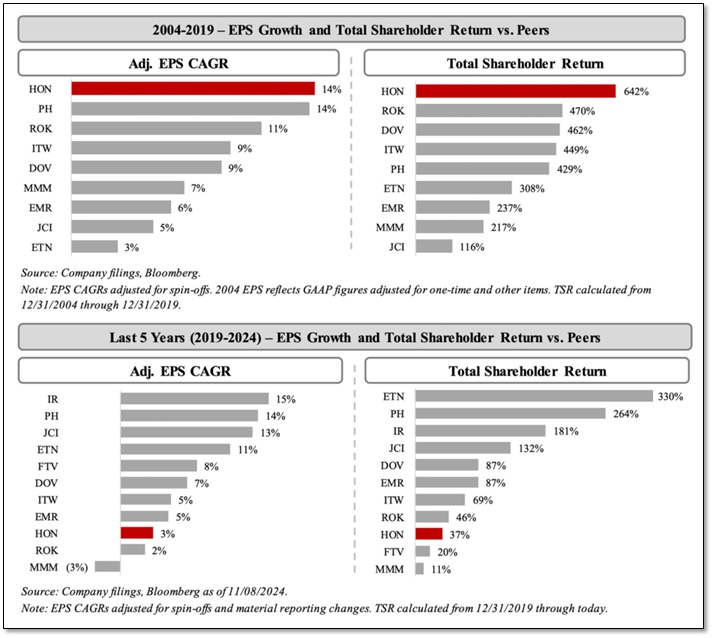

FIGURE 1: EPS Growth and Total Shareholder Return vs. Peers 2004-2019 and 2019-2024

Performance Criticism

The activist investor believes that separating Honeywell’s aerospace and automation businesses could increase the share price by 51% to 75% over the next two years and create two $100 billion companies. Over the last five years, Honeywell’s stock rose by 28%, compared to a 94% increase in the S&P 500.

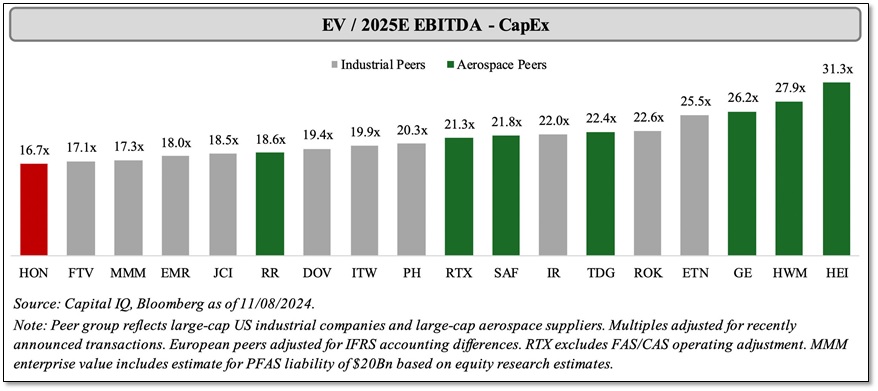

Elliott values Honeywell and its peers using EV / EBITDA – CapEx as they believe that this method accounts for Honeywell’s relatively lower capital intensity, the peer group’s different capital structures, and is the “best measure” of determining segment-level cash flow.

According to Elliott’s valuation metric, Honeywell trades today at a discount to its industrial and aerospace peers and a historically cheap level.

Elliott wrote in a letter to Honeywell’s board, “Uneven execution, inconsistent financial results, and an underperforming share price have hurt Honeywell’s strong record of value creation,” while still praising the company’s products and technology.

FIGURE 2: EV / 2025E EBITDA – CapEx

Financial Performance and Future Plans

In the third quarter, Honeywell reported that its revenue grew, but its net income fell slightly, even though its earnings per share exceeded analyst expectations. Its board approved an increase in its annual cash dividend, raising it to $4.52 per share from $4.32 per share.

Last month, Honeywell announced its plan to create a new publicly traded company from its advanced materials unit by early 2026. Additionally, it recently advised that it is looking to sell its personal protective equipment business.

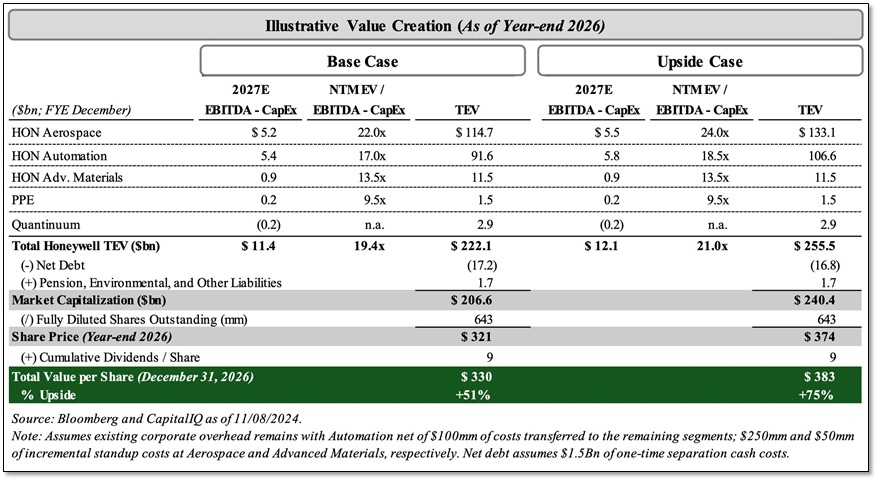

FIGURE 3: Illustrative Value Creation (As of Year-end 2016)

Honeywell’s Response

Honeywell’s board and management value the views of all shareholders. Stacey Jones of Honeywell said, “We did not know about Elliott’s views before today, but we look forward to talking with them to hear their input. Our leadership wants feedback from investors as we stick to our plan for sustainable growth, improving our portfolio, and using our capital wisely.”

Elliott’s Activism and Honeywell’s Acquisitions

Elliott manages about $70 billion in assets and is a major activist investor. It now is one of Honeywell’s largest shareholders.

It has a strong history of activism, recently pushing for changes at Southwest Airlines (NYSE: LUV) and Starbucks (NASDAQ: SBUX). A survey by Elliott found that most industrial company shareholders believe that companies focused on one area do better than those that are diversified.

This year, Elliott has started around a dozen campaigns and has been targeting larger companies than before. Its investment in Honeywell is a record high, exceeding its $3 billion investments in AT&T (NYSE: T) and SoftBank (TSE: 9434). Recently, Southwest Airlines avoided a proxy fight with Elliott by agreeing to add six new board directors. The airline also announced that Executive Chairman Gary Kelly will step down sooner.

Since Vimal Kapur became CEO of Honeywell last year, the company has made several large acquisitions. This includes a $5 billion purchase of Carrier Global’s (NYSE: CARR) security unit completed in June and Air Products’ (NYSE: APD) liquefied natural gas (LNG) unit in September.

Notes: All numbers in USD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.