Ontario has officially begun construction on Canada’s first small modular reactor (SMR), a $20.9 billion undertaking led by Ontario Power Generation (OPG) (www.opg.com) at its Darlington site. The project will ultimately consist of four SMRs based on GE Hitachi’s (www.gevernova.com) BWRX-300 design, with the first unit expected to generate power by 2030.

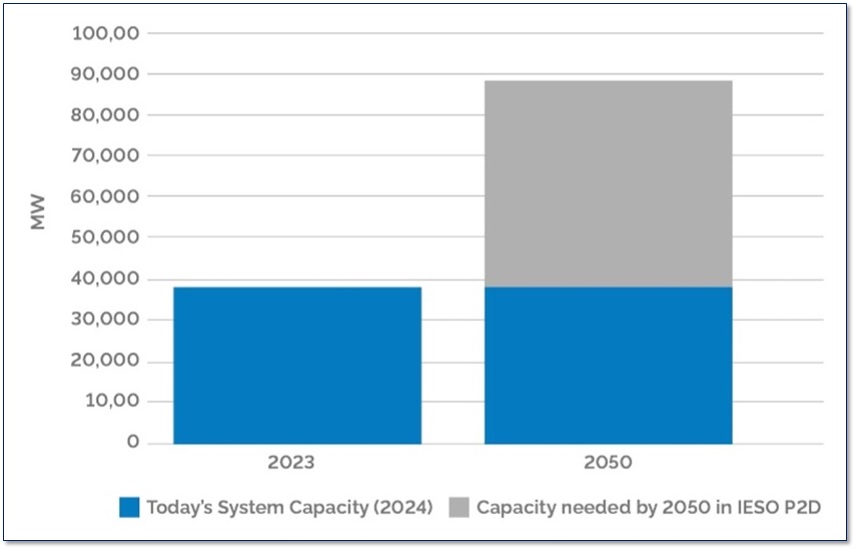

The Darlington SMR marks more than just a technological shift. It’s the province’s response to a looming 75% jump in electricity demand by 2050, and it positions Ontario and OPG as early movers in a sector that may soon see global uptake. For investors looking at nuclear exposure or broader electrification plays, the implications stretch across infrastructure, supply chains, and long-term power pricing.

The Numbers Behind the Reactors

Construction of the first reactor comes with a $6.1 billion price tag, plus $1.6 billion for common infrastructure that will serve all four units. OPG plans to finance the build through a combination of cash and debt, not taxpayer dollars, though the province continues to subsidize electricity rates through other means. In 2024 alone, Ontario budgeted $7.3 billion for hydro subsidies.

At full buildout, the SMRs will generate 1,200 megawatts, supplying power to roughly 1.2 million homes. According to the Independent Electricity System Operator (IESO), matching this output with renewables like wind or solar, along with battery storage, would cost more per kilowatt-hour and require significantly more land and transmission infrastructure.

That price point matters. The IESO estimates SMR-generated electricity will cost 14.9 cents per kilowatt-hour over its lifetime, higher than wind and solar in ideal conditions, but with fewer land, siting, and intermittency challenges.

FIGURE 1: Ontario Electricity System Capacity Requirements 2050 vs 2023

Jobs, Steel, and GDP

From a macro view, the project’s economic footprint is substantial. The government projects that construction and operation will generate $38.5 billion for Canada’s GDP over the next 65 years. That includes 18,000 construction-phase jobs and 3,700 permanent roles in operations, engineering, and skilled trades.

The Ontario government and OPG committed 80% of project spending to Ontario firms, and more than 80 Ontario companies have already inked supply contracts. These range from E.S. Fox (esfox.com) in Niagara Falls to Aecon Group (TSX: ARE), which is contributing engineering and fabrication services. GE Hitachi’s involvement brings an international angle, although only 5% of the project spend is expected to flow to U.S.-based firms.

That level of domestic participation gives Ontario a manufacturing advantage. It also sets up future export opportunities, as jurisdictions in Alberta, Saskatchewan, and New Brunswick, and even countries like Poland, Romania, and the U.K., look to Ontario’s build as a blueprint.

A Policy-Driven Project

This isn’t just about engineering, as the Darlington SMR is the product of years of political and regulatory groundwork. The current Ontario government has made nuclear power a central piece of its energy vision, citing it as key to maintaining affordable rates while electrifying Ontario’s industrial and residential sectors.

Stephen Lecce, Ontario’s Minister of Energy and Mines, was blunt during the project’s announcement: “As it stands today, we just don’t have the supply to meet [future] demand.” The province is facing new electricity loads from EV battery plants, green steel production, mining, and AI data centers. Without new baseload power, growth could stall.

According to Lecce, the Darlington project represents “the best, most affordable option to meet the growing demand,” with the province already locked into future builds at Bruce Power and Wesleyville.

FIGURE 2: Ontario’s SMR Supply Chain

Potential Risks and Skepticism

Not everyone is sold. Some environmental advocates have raised concerns about the project’s cost assumptions, pointing to the track record of nuclear developments globally. They argue that no nuclear project, particularly those involving new and unproven reactor designs, has stayed within its original budget.

Still, OPG’s track record has lent the SMR rollout some credibility. The company completed its Darlington refurbishment 169 days ahead of schedule, and the government has leaned heavily on that performance to justify its confidence in managing the SMR timeline and budget.

What It Means for Investors

For equity investors, the key players are likely to include:

- Ontario Power Generation (OPG): Not publicly traded, but an important utility to watch for bond issuance and partnerships.

- GE Hitachi: A joint venture between General Electric (NYSE: GE) and Hitachi (TSE: 6501 | OTC: HTHIY). It is leading the reactor design for the BWRX-300, and its role in the Darlington SMR project could open future opportunities in global SMR technology licensing.

- Aecon Group Inc. (TSX: ARE): Publicly traded and directly involved in nuclear infrastructure. Already a contractor for the Darlington refurbishments.

- AtkinsRéalis Group Inc. (TSX: ATRL) (fka SNC-Lavalin Group): While not directly tied to the SMR project, it owns Candu Energy Inc., a key player in Canada’s nuclear sector, and its history in CANDU reactor development and nuclear engineering may bring future roles.

- Canadian suppliers in steel, fabrication, and modular assembly: These may not be household names, but could see substantial long-term upside as SMR supply chains expand globally.

The SMR story also plugs into broader energy transition themes. The push for electrification across vehicles, homes, and industry means the demand case for nuclear is no longer theoretical. For investors tracking battery storage, grid tech, or utilities with exposure to Ontario, this project is now a reference point.

Looking Ahead

The first unit is scheduled to be completed by 2029 and online by 2030. If the rest of the project stays on schedule and within budget, the Darlington SMR could shift the conversation around nuclear economics.

Still, risks remain as delays, cost overruns, and political turnover could all impact execution. But if it succeeds, the Darlington build could set a precedent, not just for Canada, but for any country trying to meet rising power demand without betting the grid on intermittent renewables alone.

For now, it’s a project to watch. One that blends politics, engineering, and macroeconomics into a $20.9 billion litmus test for the future of nuclear energy.

Notes: All numbers in CAD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor.

The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.