![]()

![]() An original article by Lorimer Wilson, Managing Editor of munKNEE.com – Your KEY To Making Money!

An original article by Lorimer Wilson, Managing Editor of munKNEE.com – Your KEY To Making Money!

NVIDIA Corporation (NASDAQ: NVDA) is a chipmaker that pioneered graphics processing units, or GPUs which act as accelerators for central processing units, or CPUs, made by other companies (i.e. fabless). It’s working on “supercomputers” combining its own CPUs and GPUs. It currently is the leader in artificial intelligence (AI) chips, but competition is rising.

This article analyzes NVIDIA’s strategic positioning within the AI sector and its financial health, as reflected by key indicators. We will examine:

- Its relationship to AI within its business operation,

- The Company’s current market capitalization,

- The impressive YTD stock price appreciation,

- A breakdown of NVIDIA’s valuation metrics (see definition of each metric below) consisting of its most recent:

- Forward Price-to-Sales Ratio (PSR),

- Forward Price-to-Earnings (PE) Ratio,

- Forward Price-to-Earnings Growth (PEG) Ratio and

- Enterprise Value-to-Earnings Before Interest Taxes, Depreciation and Amortization (EV/EBITDA) Source.

Please note that the metrics change daily as stock prices change. Stock price and valuation metrics are based on NVDA’s stock price as of the close of business on Friday, November 3, 2023.

NVIDIA: Up 208% YTD

- NVIDIA has introduced a platform to construct quantum algorithms by employing widely known classical computer coding languages which have the ability to choose whether to run the algorithm on a classical computer or quantum computing based on efficiency,

- The Company is the leading designer of graphics processing units required for powerful computer processing,

- It is leveraging its software developed for GPUs to support the development of Quantum Computing. It has released cuQuantum, a software development kit designed to help software developers build workflows on QC, and is working on a QC software stack, as well as a hybrid QC unit in partnership with start-up Quantum Machines and

- It designs the best-in-class graphics card for AI and machine learning processing and compute and networking solutions.

- Market Capitalization: $1.07T;

- Forward PE Ratio: 45.4 (sector median is 24.5);

- Forward PSR: 19.9 (sector median is 2.4);

- Forward PEG Ratio: 1.2 (sector median is 1.7)

- EV/EBITDA Ratio: 38.2 (sector median is 13.2)

Can NVIDIA Sustain its Growth

So far in 2023, NVIDIA has experienced a phenomenal surge in both sales and stock market performance, attributing its success to its pivotal role in the ever-expanding AI sector BUT, according to the results of research conducted by Research Affiliates, the investment firm headed by Robert Arnott, it is rare for the largest companies to still be among the largest in a decade’s time.

He and fellow researchers focused on the 10 largest-cap companies at the beginning of each decade since 1980. They found that, on average, eight of those 10 were gone from the top-10 list by the end of that decade. Furthermore, the average 10-year performance of all 10 was significantly below that of the overall U.S. market. (Source)…What accounts for this result? There are several contributing factors:

- Overvaluation: It’s almost certain that the largest-cap stocks are, on average, overvalued. They are the largest because they are riding a wave of investor sentiment and enthusiasm. Unless you believe that overvaluation doesn’t exist, it’s far more likely to occur among stocks that are in favor than those that are out of favor.

- Competition: In a 2012 study entitled “The Winners Curse,” Arnott and Lillian Wu, also of Research Affiliates, wrote that “When you are #1, you have a bright bull’s-eye painted on your back. Governments and pundits are gunning for you. Competitors and resentful customers are gunning for you. Indeed, in a world of fierce competition and serial witch hunts in the halls of government, that target is probably painted on your front and sides too. In a world that generally roots for the underdog, hardly anyone outside of your own enterprise is cheering for you to rise from world-beating success to still-loftier success.”

- Law of diminishing returns: Many of the largest companies are trading on investors’ assumption that they will continue growing at impossibly fast paces, despite already being huge. However, it becomes harder and harder to grow at a fast pace the larger a company becomes. Furthermore, even if one of these mega-cap companies could grow at the necessary pace, which is in itself unlikely, it’s mathematically impossible that all of them will be able to, since that would mean that in several years’ time, they collectively would be bigger than the economy as a whole.

The bottom line? Regardless of how NVIDIA [as one of the ‘Magnificent Seven’] has performed YTD its long-term prospects are mediocre at best. As Arnott wrote in an email: “Whoever coined the expression ‘Magnificent Seven’ presumably didn’t see the movie, where four of the seven are dead by the end of the film.” (Source)

Luke Lango points out that, while NVDA stock was the No. 1 AI stock to buy in 2023, he thinks it could turn into the No. 1 AI stock to sell. He reasons that because NVIDIA has benefitted from a huge demand surge in 2023, primarily because Big Tech firms were looking to build new AI models with its GPUs, that surge will prove temporary because those same Big Tech firms that have been fueling the surge are now moving away from NVIDIA to develop their own chips. Source

Commentary

According to an October 31 report by the Wall Street Journal NVDA faces the risk of $5 billion in orders for its advanced chips to the Chinese market being canceled due to newly implemented US regulations….NVIDIA had already finished delivering orders of its sophisticated AI chips to China for 2023 and was attempting to make advance deliveries for some of its 2024 orders before the new export controls came into force in mid-November, per WSJ…[but] NVIDIA was informed by the US government last week that the new export restrictions targeting the sale of high-end chips to other countries, including China, were effective immediately….The restrictions are part of the broader Biden administration’s strategy to limit China’s access to advanced technology, which it believes could enhance China’s military and cyberwarfare capabilities….[To offset] the impact of the new export controls, NVIDIA’s spokesman said that the Company has been actively engaged in efforts to distribute its advanced AI computing systems, which utilize graphics chips impacted by the regulations, to customers within the United States and other regions. (Source)

According to CNBC’s Jim Cramer, however, the latest U.S. restrictions on AI chip sales in China won’t dethrone NVIDIA as the world’s most valuable semiconductor company but, rather spells trouble for rivals Advanced Micro Devices and Intel as it will heat up competition in the U.S. market further. (Source)

FQ2/2024 Financials for the second quarter ended July 30, 2023

(The AI chip leader plans to report earnings for its fiscal third quarter on Nov. 21.)

| Non-GAAP | |||||

| ($ in millions, except earnings per share) | FQ2/2024 | FQ1/2024 | FQ2/2023 | Q/Q | Y/Y |

| Revenue | $13,507 | $7,192 | $6,704 | Up 88% | Up 101% |

| Gross margin | 71.2% | 66.8% | 45.9% | Up 4.4 pts | Up 25.3 pts |

| Operating expenses | $1,838 | $1,750 | $1,749 | Up 5% | Up 5% |

| Operating income | $7,776 | $3,052 | $1,325 | Up 155% | Up 487% |

| Net income | $6,740 | $2,713 | $1,292 | Up 148% | Up 422% |

| Diluted earnings per share | $2.70 | $1.09 | $0.51 | Up 148% | Up 429% |

Outlook

NVIDIA’s outlook for the third quarter of fiscal 2024 is as follows:

- Revenue is expected to be $16.00 billion, plus or minus 2%.

- GAAP and non-GAAP gross margins are expected to be 71.5% and 72.5%, respectively, plus or minus 50 basis points.

- GAAP and non-GAAP operating expenses are expected to be approximately $2.95 billion and $2.00 billion, respectively.

- GAAP and non-GAAP other income and expense are expected to be an income of approximately $100 million, excluding gains and losses from non-affiliated investments.

- GAAP and non-GAAP tax rates are expected to be 14.5%, plus or minus 1%, excluding any discrete items. (source)

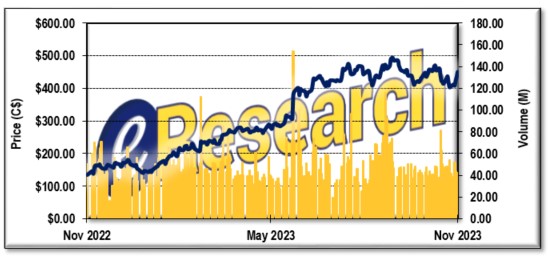

Figure 1: NVIDIA’s 1-Year Stock Chart

Definitions:

- The price-to-sales ratio (PSR) describes how much someone must pay to buy one share of a company relative to how much that share generates in revenue for the company. and, as such, determines whether its stock is cheap or overpriced in comparison to its peers. The mean forward sector ratio is considered excellent when the value falls below two (2). The mean forward PSR for Information Technology-Semiconductor companies is 2.4.

- The Enterprise Value-to-Earnings Before Interest, Taxes, Depreciation, and Amortization ratio (EV/EBITDA) is one of the best metrics used by value investors to evaluate a company because it accounts for the value of all financing the company has received from both equity stakes and debt allowing investors to compare profitability between companies. A high means the company is overvalued, while a low ratio indicates it’s undervalued. The mean forward EV/EBITDA ratio for Information Technology-Semiconductor companies is 13.2.

- The price/earnings to growth ratio (PEG ratio) is considered to be an indicator of a stock’s true value. A PEG lower than 1.0 is best, suggesting that a company is relatively undervalued. The Information Technology-Semiconductor sector median ratio is 1.7.

Notes: All numbers in USD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.