![]()

![]() eResearch | After recently listing, Arm Holdings plc (NASDAQ: ARM) is struggling to find footing in a declining market and sentiments that the semiconductor stocks are overvalued.

eResearch | After recently listing, Arm Holdings plc (NASDAQ: ARM) is struggling to find footing in a declining market and sentiments that the semiconductor stocks are overvalued.

Arm debuted on September 13, 2023. The initial public offering (IPO) price for Arm was set at $51 per share. On the first day of trading, Arm’s stock price opened at $56.10 and closed the day at $63.59 per share, a first-day gain of approximately 25% above its IPO price.

In terms of the funds raised through the IPO, Arm sold approximately 95.5 million American Depositary Shares (ADS) at the IPO price of $51 per share. The IPO raised net proceeds of approximately $4.68 billion, making it the largest IPO this year and one of the noteworthy technology sector IPOs in recent years.

Billion Dollar IPO but the Cash Goes to Softbank

The Company will not receive any proceeds from the offering, as SoftBank sold the shares and still controls over 90% of the outstanding shares of Arm. However, Arm held over $2 billion in cash and short-term investments, as of the end of June, to fuel its operations.

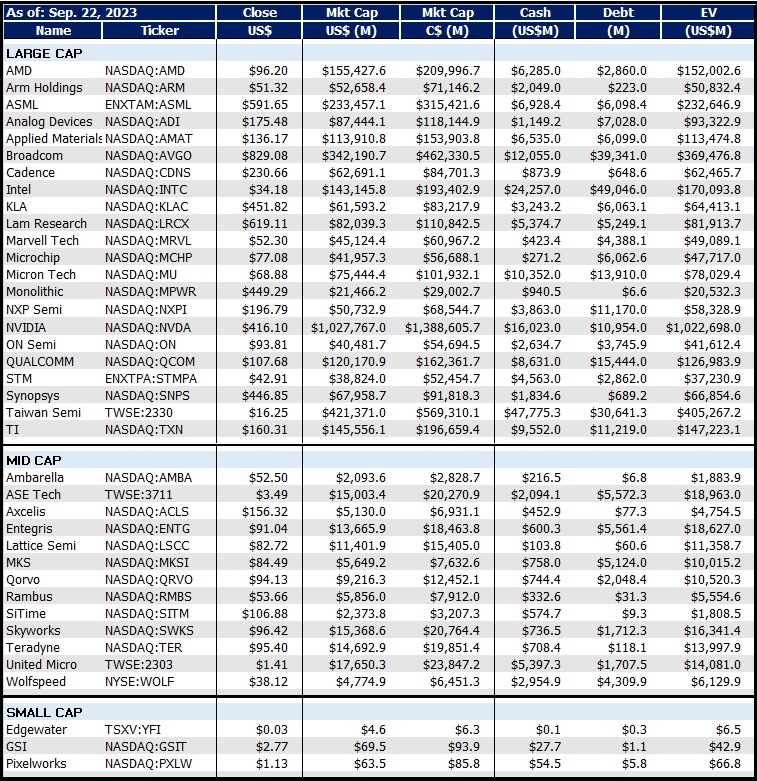

In 2016, SoftBank took Arm private in a $32 billion acquisition. The valuation of Arm at the time of its IPO was nearly $60 billion when it began trading and is currently around $53 million (see Figure 1).

In September 2020, SoftBank announced its intention to sell Arm to NVIDIA for $40 billion, subject to regulatory approvals. However, the proposed acquisition raised regulatory concerns in the EU, UK, and the US, and the deal never closed.

FIGURE 1: Market Comps

Partners and Competitors Wanted in on the IPO

According to the Arm’s prospectus, investor interest in the IPO was substantial. Strategic investors, including major technology companies like AMD, Apple, Cadence, Google, Intel, NVIDIA, Samsung, and Taiwan Semiconductor, participated in the IPO by purchasing $735 million worth of Arm shares.

Arm’s successful IPO and strong investor interest underscored its strategic importance in the semiconductor ecosystem and its potential for continued growth and innovation in the technology sector.

Arm’s business has fared better than the broader chip industry because it licenses designs rather than paying to make processing systems itself.

Arm Stock Price Declines on Second Week Jitters and Analysts’ Tepid Outlooks

During the second week of trading, Arm’s stock price dropped more than 15.5%. In comparison, the NASDAQ market exhibited a decline during the same timeframe of only 3.2%.

While Arm’s performance lagged behind the broader NASDAQ market, it is important to note that individual stock performance can be influenced by various company-specific factors, market dynamics, and investor sentiment, which may not always align with broader market trends.

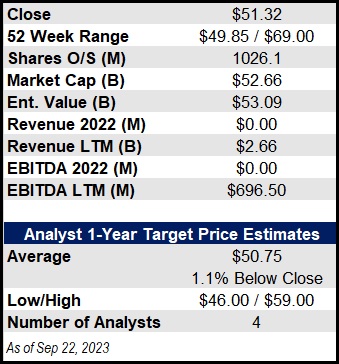

In addition, equity analysts from the sell-side initiated coverage of Arm following its IPO.

- The Susquehanna analyst assigned a “neutral” rating to Arm with a price target of $48 per share.

- The Bernstein analyst issued an “underperform” rating with a $46 price target.

The consensus among analysts appears to be cautious, with a focus on valuation and growth prospects. It is important to note that “Neutral” and “Underperform” ratings are relatively less common compared to “Buy” recommendations. These ratings suggest a level of uncertainty or skepticism regarding Arm’s stock performance. The consensus pricing from analysts reflects a moderate outlook, with price targets in the range of $46 to $48 per share, indicating a potential downside from the IPO price (see Figure 2).

FIGURE 2: Analysts Target Prices

Financials Not Supporting the Growth Thesis.

In Fiscal 2023 (F2023), ending on March 31, 2023, Arm’s revenue was $2.679 billion, relatively flat when compared to the preceding fiscal year when it reported revenue of approximately $2.703 billion.

In terms of profitability, Arm achieved a gross profit margin of 96%, and an operating income margin was reported at 25%, reflecting a healthy level of overall profitability. Net income was $524 million during F2023, down from $549 million in the previous fiscal year.

In the first fiscal quarter (FQ1/2023) ending June 30, 2023, Arm reported revenue of $675 million, which was down 2.5% year-on-year.

The Company also reported the number of Arm-based chips that customers shipped at 6.844 billion, down from 7.314 billion in FQ1/2022.

Net Income in the first fiscal quarter was also down to $105 million from $225 million in the same period last year.

So, in terms of year-on-year growth from FQ1/2022 to FQ1/2023, Arm saw a decline in revenue, number of Arm-based chips shipped, and net income.

Arm’s ability to maintain a high gross profit margin suggests that its business model, which revolves around licensing intellectual property and designs, allows for cost-effective revenue generation. However, the stability in revenue and moderate growth in net income indicate that Arm may be operating in a mature market with limited growth potential during that specific fiscal year.

Valuation Multiples in the Irrational Exuberance Range

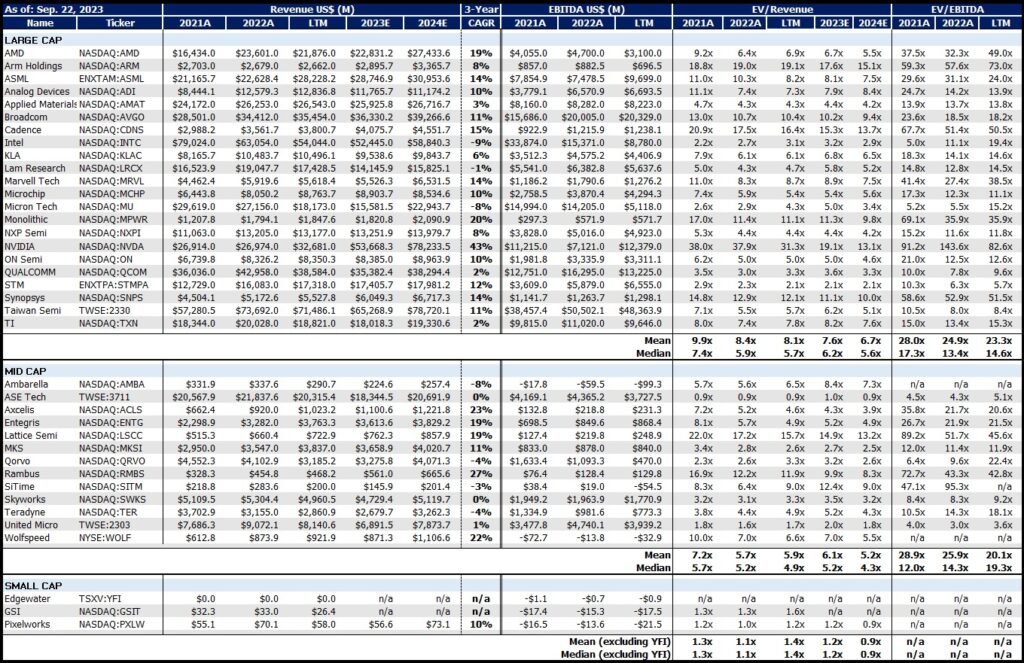

Valuation multiples are commonly used to compare the financial performance and value of companies in the same industry. One of the most popular valuation multiples is the Enterprise Value (EV) to Revenue (EV/Revenue) ratio, which measures how many times a company’s revenue can cover its total enterprise value.

According to S&P Capital IQ, the average EV/Revenue multiple for the large-cap companies in the semiconductor industry, using revenue estimates for 2023, was 7.6x. This means that the average semiconductor company had an Enterprise Value of 7.6x its revenue.

However, this multiple can vary significantly depending on the size, profitability, growth prospects, and competitive position of each company, and ranged from 2.1x to 19.1x for the large-cap companies with NVIDIA, Arm, and Cadence at 19.1x, 17.6x, and 15.3x, respectively (see Figure 3).

FIGURE 3: Valuation Comps

Arm’s Strategic Advantages

Arm is a leading player in the design and licensing of semiconductor intellectual property (IP), with a particular focus on Central Processing Unit (CPU) architecture. The company’s business model revolves around creating high-performance, energy-efficient CPU designs and related technology, which are then licensed to semiconductor companies and original equipment manufacturers (OEMs). These licensees leverage Arm’s IP to develop their own chips, ranging from mobile devices to data centers and IoT applications.

Arm’s CPU designs have gained prominence due to their energy efficiency, making them suitable for a wide range of devices where power consumption is a critical factor. The Company’s CPUs are ubiquitous in the semiconductor industry and play a pivotal role in enabling advanced computing across various sectors.

In addition to CPU IP, Arm offers complementary products such as GPUs (Graphics Processing Units), System IP, and compute platforms. These products enable the efficient creation of system-level solutions for increasingly sophisticated devices and applications.

Arm’s business model is characterized by flexibility and scalability. Licensees can customize Arm’s CPU designs to meet their specific performance and power requirements, leading to economies of scale and cost-effectiveness.

Arm and AI

Arm believes it can play a pivotal role in the shift toward AI and machine learning (ML)-driven computing, with its CPUs powering AI workloads in billions of devices worldwide.

In emerging areas like large language models, generative AI, and autonomous driving, Arm is focusing on energy-efficient acceleration for these algorithms. The Company’s commitment to enhancing CPUs and GPUs with specialized functionality underscores its contribution to advancing AI and ML capabilities across diverse devices and applications.

Capturing Part of a Billion Dollar Market

Arm operates in a highly competitive and ever-changing semiconductor market. The Company’s CPUs and IP solutions are integrated into a wide range of electronic devices and solutions, including automotive systems, data servers, digital TVs, Internet of Things (IoT) devices, networking equipment, personal computers (PCs), smartphones, and tablets.

Arm estimates its Total Addressable Market (TAM) at approximately $202.5 billion, with a projected CAGR of 6.8% to reach about $246.6 billion by December 31, 2025. According to the Company, its technology was integrated into chips valued at around $98.9 billion in 2022, signifying a 48.9% market share, compared to 42.3% in 2020.

Arm’s CPUs are particularly well-suited for mobile devices, where energy efficiency is critical. As such, the Company has established a dominant position in the mobile device market, powering over 99% of the world’s smartphones. Moreover, its CPUs are increasingly used in data centers and emerging technologies like IoT and automotive applications.

The Company anticipates a growing role in chip technology, resulting in higher royalties relative to total chip value as chip design complexity continues to rise.

Competitors Not Standing Still

Arm faces competition from several notable competitors in the semiconductor and CPU design space. Some of its key competitors include:

- NVIDIA:

- NVIDIA specializes in GPUs but has also ventured into CPU designs. It tried to buy Arm in 2020.

- Recently the use of NVIDIA’s solutions in AI has caused its stock price to increase substantially.

- Intel:

- Intel is a major player in the semiconductor industry, known for its x86 CPU architecture in most PCs.

- It competes with Arm, especially in the data center and PC markets.

- Qualcomm:

- Qualcomm is a leading provider of mobile chipsets, including Snapdragon processors, competing directly with Arm in the mobile device market.

- Advanced Micro Devices (AMD):

- AMD is known for its x86 CPUs and GPUs and competes with Arm in various segments, including data centers and PCs.

- RISC-V:

- RISC-V is an open-source CPU architecture gaining traction, posing a potential competitive threat to proprietary CPU designs like Arm’s.

Market Trends in the Semiconductor Industry

Arm, with its focus on energy efficiency and adaptable CPU designs, is well-positioned to address current market trends and maintain its relevance in the semiconductor industry.

The current market trends in the semiconductor industry include:

- AI and ML Acceleration:

- The demand for AI and machine learning capabilities in semiconductor devices is growing rapidly. Companies are focusing on designing CPUs and accelerators optimized for AI workloads.

- IoT Growth:

- The IoT is driving the need for energy-efficient and compact semiconductor solutions for a wide range of IoT devices.

- 5G Connectivity:

- The rollout of 5G networks is fueling demand for semiconductor components in 5G-enabled devices and infrastructure.

- Supply Chain Challenges:

- The industry is grappling with supply chain disruptions, impacting semiconductor manufacturing and distribution.

- Eco-Friendly Solutions:

- Sustainability is a growing concern, leading to the development of energy-efficient and environmentally friendly semiconductor technologies.

Final Thoughts

The semiconductor market is characterized by rapid technological advancements and evolving consumer demands. As a result, Arm faces continuous competition from other CPU and semiconductor IP providers, both established players and emerging startups. The Company’s ability to innovate and adapt to changing market trends is critical to its sustained success.

Notes: All numbers are in USD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.