eResearch is pleased to publish an Update Report on EQ Inc. (TSXV:EQ). The report covers the Company’s Q1/2022 Financial Results and recent news.

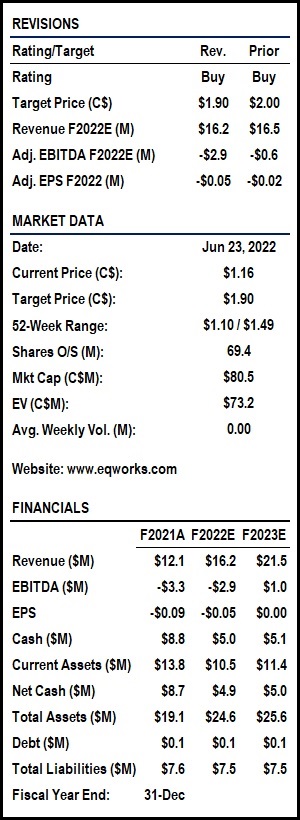

We are maintaining our Buy rating but decreased our one-year price target to $1.90 from $2.00 after changes to our valuation calculation. In our DCF valuation calculation, we lowered the Terminal EBITDA multiple in 2027 to 15x from 16x. In the Revenue Multiple valuation calculation, we lowered the revenue multiple to 5.0x from 6.0x to keep both metrics in-line with comparable companies.

You can download the full 12-page report by clicking here: eR-EQ-UR-2022-Q1-2022-06-23_FINAL

EQ enables businesses to understand, predict, and influence customer behaviour. Using unique and third-party data sets, advanced analytics, artificial intelligence, and machine learning, EQ creates actionable intelligence for businesses to attract, retain, and grow customers.

The Company’s proprietary SaaS platform mines insights from location and geospatial data, enabling businesses to close the loop between digital and real-world consumer actions. EQ is one of the largest providers of location-based data in Canada with over 1 petabyte of data.

Quarterly Highlights:

Quarterly Revenue Up 55% Y/Y

Quarterly Revenue Up 55% Y/Y- EQ reported a 54.6% Y/Y revenue increase to $2.7 million in Q1/2022, recording its highest first-quarter revenue in a decade, but slightly below our estimate of $3.0 million.

- However, revenue dropped Q/Q as the Company’s services are affected by seasonality as Q1 is traditionally the lowest revenue quarter of the year as approximately 35% of EQ’s revenue occurs in Q4 due to increased advertising activity during the North American holiday season.

- The Company’s Advertising Services segment revenue rose 67% Y/Y to $2.1 million, while the Data Sales segment revenue rose almost 22% Y/Y to $0.6 million.

- Data Business Continues to Grow, 22% Higher Y/Y

- The Y/Y revenue increase was powered by clients’ new data engagements and the Company’s continued focus on automotive, financial services, and retail industries. Moreover, the reopening of retail businesses and more advertisement spending also contributed to the improved quarterly performance Y/Y.

- EQ expects to launch several proprietary SaaS data products during the second half of 2022 that could generate “meaningful results” towards the end of 2022 and into 2023.

Revenue Guidance:

- EQ continued to build its product offerings by investing in its consumer-facing application (Paymi) with unique zero-party data assets and propriety technology products, in addition to recruiting data scientists, sales executives, and marketing personnel.

- Paymi’s acquisition adds a new revenue stream and facilitates expansion into multiple new customer verticals. The propriety technology platform accumulates first-party data (100% consent-based) and should enhance the Company’s LOCUS (analytics and AI framework) platform with proprietary zero-party data.

- The Company reportedly has seen significant traction and interest from clients across multiple verticals and it continues to focus on its key verticals – automotive, financial services, and retail industries. Furthermore, the Company expects to launch several proprietary SaaS data products during the second half of 2022 that could generate “meaningful results” towards the end of 2022 and into 2023.

Financial Analysis & Valuation:

- Due to a slower launch of EQ’s new data services, we have lowered our quarterly revenue estimate to $3.5 million in Q2/2022 from $4.0 million but increased our quarterly revenue estimate to $5.5 million in Q4/2022 from $5.0 million. For 2022, we are slightly reducing our 2022 revenue estimate to $16.2 million from $16.5 million based on the lower revenue in Q1/2022.

- In our DCF valuation calculation, we lowered the Terminal EBITDA multiple in 2027 to 15x from 16x. In the Revenue Multiple valuation calculation, we lowered the revenue multiple to 5.0x from 6.0x to keep both metrics in-line with comparable companies.

- We estimate an equal-weighted price target of $1.90 based on a DCF valuation ($2.35/share) and Revenue Multiple valuation ($1.45/share).

We are maintaining our Buy rating and reducing our one-year price target to $1.90 from $2.00.

You can download the full 12-page report by clicking here: eR-EQ-UR-2022-Q1-2022-06-23_FINAL

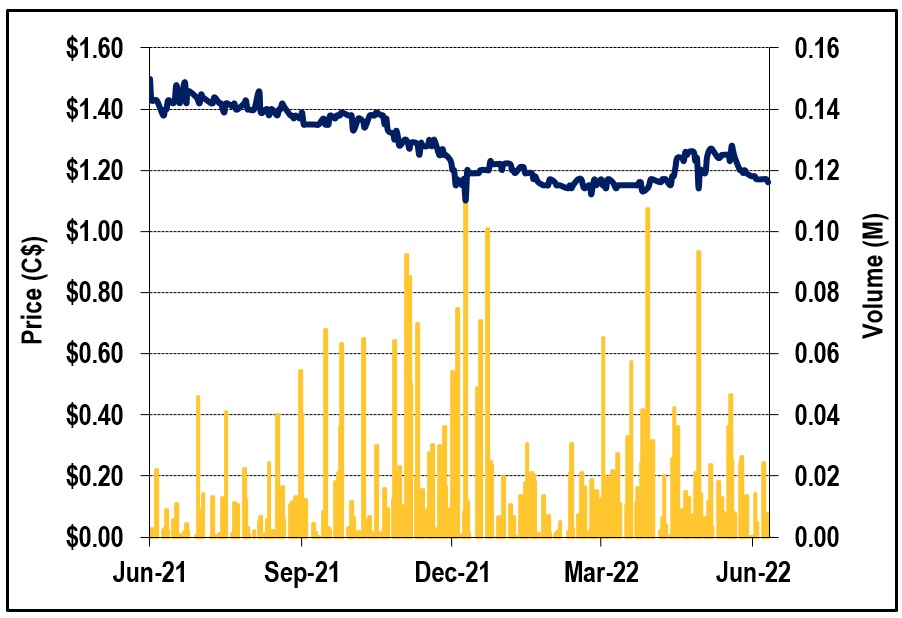

FIGURE 1: EQ 1-Year Stock Chart

Notes: All numbers in CAD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.