eResearch| Square (NYSE:SQ) recently announced its plans to acquire the Australian Fintech company, Afterpay (ASX:APT) for an implied value of approximately USD$29 billion (AUD$39 billion) in a share-swap deal.

![]()

![]() As part of the agreement between the two companies, Square will acquire all issued shares of Afterpay and pay a 30% premium for the transaction.

As part of the agreement between the two companies, Square will acquire all issued shares of Afterpay and pay a 30% premium for the transaction.

The deal value Afterpay at 30.5 times Enterprise Value to Revenue (EV/Revenue) and 218.2 times Enterprise Value to EBITDA (EV/EBITDA).

Both Square and Afterpay have witnessed strong growth during the pandemic. Square earned revenue of $15.9 billion for the twelve months ended June 30, 2021, an increase of over 170% year-over-year. For Fiscal 2020, for the year ended June 30, 2020, Afterpay booked revenue of A$519.2 (US$372.9) million, an increase of nearly 103% as compared to 2019.

The deal comes amid a rapidly growing trend of Buy-Now-Pay-Later (BNPL) services, allowing customers to buy goods or services by paying part of the purchase price at the time of purchase and the remaining balance in a series of installments instead of credit checks.

Afterpay is considered a pioneer in the industry and Square wants to make use of this popular payment platform to add to and improve its offerings. The deal is expected to close in the first quarter of 2022, provided that certain closing conditions are met.

Square-Afterpay Acquisition Potential

The acquisition is primarily targeted towards broadening the combined company’s products and services, making them more compelling, adding new users to their customer base, and generating incremental revenue for even the smallest of merchants.

The acquisition is primarily targeted towards broadening the combined company’s products and services, making them more compelling, adding new users to their customer base, and generating incremental revenue for even the smallest of merchants.

Capitalizing on Afterpay’s BNPL services, Square plans to accelerate strategic priorities for its Seller and Cash App ecosystems and integrate Afterpay into these business units, enabling merchants of all sizes to offer “buy now and pay later” at checkout.

Jack Dorsey, Co-Founder and CEO of Square, stated “Square and Afterpay have a shared purpose. We built our business to make the financial system more fair, accessible, and inclusive, and Afterpay has built a trusted brand aligned with those principles. Together, we can better connect our Cash App and Seller ecosystems to deliver even more compelling products and services for merchants and consumers, putting the power back in their hands.”

BNPL: A Trend that has Grown during COVID-19 Pandemic

During the economic tough times caused by the COVID-19 lockdown, loss of income and financial uncertainty forced people to conserve cash and look for alternative methods to borrow money.

Services that didn’t charge any interest witnessed a growing demand, especially among younger users, many of whom lost jobs.

BNPL services offer a similar solution as the merchant pays commission to the BNPL provider, provided that the user clears the balance before the delay period is up.

BNPL also presents an opportunity for businesses to tackle changing consumer payment behavior from traditional credit to better and more convenient online payment methods.

BNPL is emerging as an effective alternative to credit cards as it allows consumers to shop and pay at a later date with benefits like zero interest and instant settlement.

From a security perspective, BNPL has an edge over credit cards as users are not required to enter the card or bank details every time they are making a payment online. Thus, they are not subject to phishing or account hacking scams.

BNPL Services: Market Overview

The BNPL sector has seen rapid growth in the last few years. As the shift to electronic payment methods and online shopping accelerated, the value of BNPL transactions continued to grow strongly.

Industry leaders, such as Afterpay, Klarna, and Affirm have been able to acquire new customers and expand their footprints. According to Bank of America (NYSE:BAC), the market for BNPL apps is expected to grow by 10 to 15 times its current value and be valued at between US$650 billion to US$1 trillion by 2025.

56% of Americans have used a BNPL Service

In July 2020, The Ascent conducted a survey on 2000 Americans to understand their BNPL habits and found that nearly 38% of consumers had used one of these services at least once.

When the same survey was conducted in March 2021, the results reached 56%, showing an increase of almost 50% in less than a year.

In the 18 to 24-year-old consumer group, the number jumped substantially by 62%. However, older adults (aged 55 or more) showed maximum growth, increasing by almost 98%.

Additional key findings from the survey included:

- The most common reason for people using BNPL services was affordability. Nearly 45% of respondents said that they used BNPL to make purchases that didn’t fit in their budget.

- Nearly 53% of respondents who had never used BNPL before said that they are likely to use these services in or before 2022, indicating a tremendous growth potential of the industry.

- Nearly 62% of BNPL users said that BNPL could replace credit cards.

- Since the COVID-19 outbreak, nearly 64% of Americans have used a BNPL service more than once. Out of these respondents, around 41% used them in order to conserve cash in case of an emergency

It is no surprise that the usage of BNPL services has significantly increased after the COVID pandemic. Based on the current scenario, it is likely to increase even further in the near future and forms part of the new digital payment ecosystem.

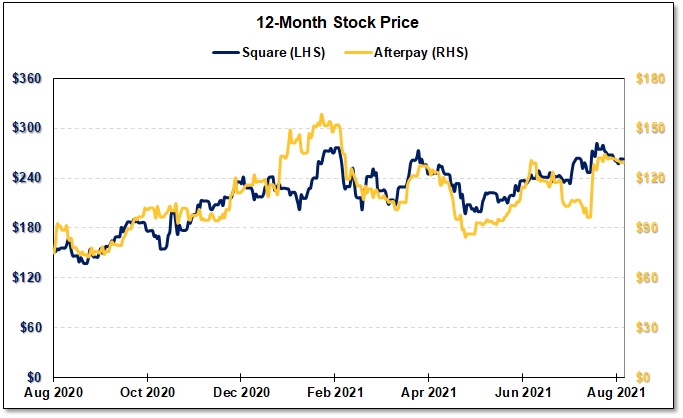

FIGURE 1: Square and Afterpay – 1-Year Stock Chart

Notes: All numbers in USD unless otherwise stated. The author of this report, and employees, consultants, and family of eResearch may own stock positions in companies mentioned in this article and may have been paid by a company mentioned in the article or research report. eResearch offers no representations or warranties that any of the information contained in this article is accurate or complete. Articles on eresearch.com are provided for general informational purposes only and do not constitute financial, investment, tax, legal, or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this information should consult with a financial advisor. The article may contain “forward-looking statements” within the meaning of applicable securities legislation. Forward-looking statements are based on the opinions and assumptions of the Company’s management as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Please read eResearch’s full disclaimer.