Below is an article written by Lorimer Wilson of Munknee.com. MunKNEE.com is a new affiliate of eResearch.com.

//

Gold has historically been the world’s best store of liquid wealth and a defense against potential devaluation of fiat currencies making it an ideal choice to complement and strengthen your portfolio. The question is: “How much gold should you own?” This article discusses a number of different views on the subject in an attempt to help you answer that question.

Written by Lorimer Wilson, editor of munKNEE.com

Asset allocation is usually taken for granted as being a mix of the three main asset classes: stocks, bonds and cash but this traditional approach is not only outdated, but also completely excludes key asset classes such as precious metals as well as foreign currency, real estate, collectibles, natural resources and life settlements.

According to Portfolio Visualizer,

- gold’s correlation with equities hovers around zero and

- gold’s correlation with bonds is around 0.3

Therefore an investment in gold works well for protecting your principal against equity bear markets and inflation. In addition, gold gives you something that you can cash in if equities and bonds go down at the same time enabling you to sustain your lifestyle without having to sell equities or bonds at unfavorable prices.

An analysis of gold’s performance since 1970 shows that gold offers potential preservation of purchasing power in varying inflationary environments:

- During periods when the annual rate of inflation in the U.S. has been below 2%, the price of gold has risen at an average annual rate of 6.7%.

- During periods of moderate inflation — defined as an annual increase between 2% and 5% — gold has risen at an average annual rate of 7.4%.

- During periods when inflation has been running above 5% a year. During such times, the gold price has increased by an average annual rate of 15.2%. Source

While gold is a smart investment, though, you should only invest a portion of your portfolio in this commodity, not because it isn’t safe to invest in gold, but because you have to build a diversified portfolio to weather the ups and downs of the stock market. Gold, like stocks, doesn’t trade perpetually higher. It fluctuates in value just like any investment so the question remains: “How much gold should you own?”

Portfolio Allocation Suggestions

Jeff Berwick: “While I would have no problem with having 100% in gold bullion in my portfolio I recommend holding:

- at least 30% of one’s portfolio in gold and silver bullion,

- an additional 20% in gold mining juniors

- and 15% in gold mining major stocks

- for a total allotment in precious metals of 65%.

Why? Because I expect all the monetary printing going on with abandon in the western world to foment a true bubble, not only in the price of gold but, even more so, in the price of the mining shares, especially the juniors where I expect a mania for the ages to unfold.” Source

Robin Cornwell asserts that physical bullion should be considered an independent asset class and an allocation to precious metal bullion, as the most uncorrelated asset group, is essential for proper portfolio diversification. Unlike Berwick, he contends that commodity stocks add uncertainty as they expose portfolios to other variables such as financial, geographic and political risks which are then layered on top of operational and management issues.

Instead, Cornwell points out, based on a study by Ibbotson Associates that, “Based on historical efficient frontiers, including precious metals moderately improved the efficient frontier and, based on forward-looking efficient frontiers, including precious metals lead to asset allocations with higher Sharpe ratios and that, as such:

- investors could potentially improve the reward-to-risk ratio:

- in conservative portfolios by allocating 7.1% to precious metals,

- in moderate portfolios by allocating 12.5% to precious metals, and

- in aggressive portfolios by allocating 15.7% to precious metals.”

In addition, he pointed out that “Ibbotson Associates found that precious metals, excluding cash, is the only asset class with a positive correlation coefficient with inflation and, therefore, the only asset class that can provide protection from a systemic crisis.” Source

Nick Barisheff puts forth that while “the percentage mix is debatable what is certain is that the historic three-asset-class allocation mix is outdated, out of touch with today’s economic and financial reality and a recipe for loss of wealth. To protect your portfolio and preserve your wealth, a 5% to 20% allocation to precious metals is an absolute necessity.”

Jeff Clark maintains that “If 10% of your total investable assets (i.e., excluding equity in your primary residence) aren’t held in various forms of gold and silver then your portfolio is at risk.”

David Ranson of Wainwright Economics, suggests that “the sensitivity of portfolio returns to the cumulative change in the price of gold is almost exactly zero at a mix of 15% gold and 85% stocks meaning that, according to our calculations, such a portfolio is almost exactly immune to the damage that inflation (as expressed by the gold price) does to stocks.” Source

Erika Nolan says “Every investor should have a minimum of 10% of their portfolio in physical gold – coins or bars.” Source

Jeffrey Christian and the CPM Group re-ran the numbers in a back-test from about 1968 to late 2016 and what they found was that if you took a portfolio of 50% S&P and 50% T-bills and you added gold to it in 5% increments, the optimal gold allocation was actually about 27% to 30% gold depending on whether you used T-bills or T-bonds respectively. Source

Richard and Robert Michaud (New Frontier Advisors): Their “resampled efficiency (RE) optimization approach to portfolio allocation analysis determined that a gold allocation between 2% & 9% will maximize risk-adjusted returns across the spectrum of risk tolerances. Broadly speaking, the higher the risk in the portfolio, whether in terms of volatility, illiquidity or concentration, the larger will be the modeled gold allocation to offset that risk. The portfolio allocation most likely to maximize returns for every unit of undertaken portfolio risk amid any combination of future financial and market conditions.” Source

Some Conclusions

Gold can be over-hyped by its most die-hard proponents, but the case for owning a little in a diversified portfolio is hard to ignore.

- U.S. stocks are at record levels exactly at a time when global stress – trade tensions, populist nationalism, and the like – appears to be growing so this may be an opportune moment for you to shift at least a portion of their portfolios to gold: both the metal and depressed mining shares.

- In addition, as the world’s financial and monetary systems become increasing fragile, saving in gold is the ultimate safe haven for protecting you against a systemic collapse. In the inevitable transition that will follow such a collapse, holding gold as wealth is the ultimate strategy for survival. Saving in gold frees your mind allowing you to sleep well at night and not worry about inflation, financial markets and currency risks.

- While gold has traditionally been seen as a tactical way to help preserve wealth during market corrections, times of geopolitical stress or persistent dollar weakness, we think there is a case to be made for gold as a core diversifying asset with a long-term strategic role in multi-asset portfolios.

//

munKNEE.com is a new affiliate of eResearch.com. To learn more about munKNEE.com, please visit their website and sign-up for their weekly newsletter.

To view the original article and more from munKNEE.com, please visit: https://www.munknee.com/how-much-gold-should-you-own-5-10-20-30-or-even-more/

//

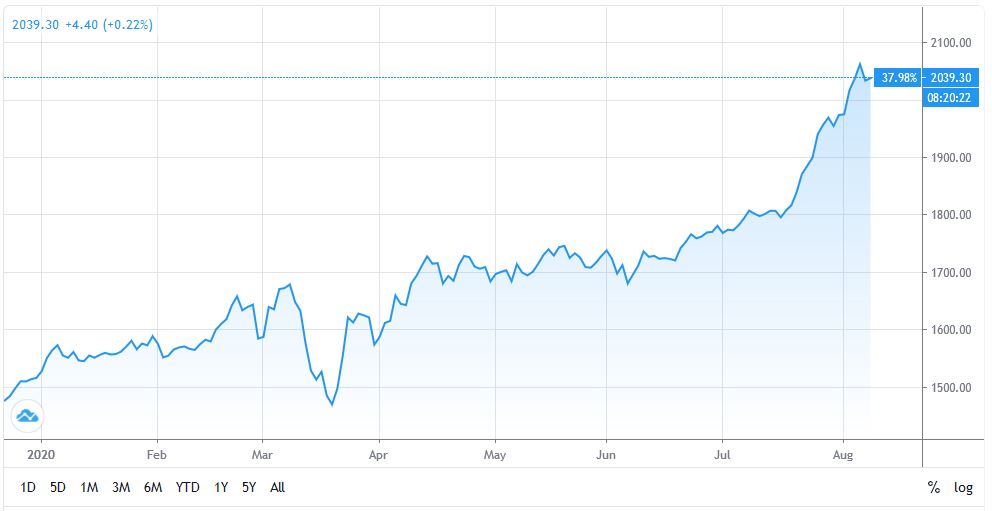

CHART 1: Gold Chart – 1 Year (up 38%)