You can download our 14-page Update Report by clicking on the following link: eR-Peak_PKK-UR-2020_05_31-FINAL

//

Peak Positioning (“Peak”) is the parent company of a group of FinTech subsidiaries operating in China’s commercial lending industry.

Peak thereby provides an investment vehicle for North American investors looking to participate in China’s FinTech industry.

Peak’s subsidiaries use technology, analytics, and artificial intelligence to provide loans, help small and medium enterprises obtain loans, help lenders find clients, and also minimize lending risk.

2019 FINANCIAL HIGHLIGHTS:

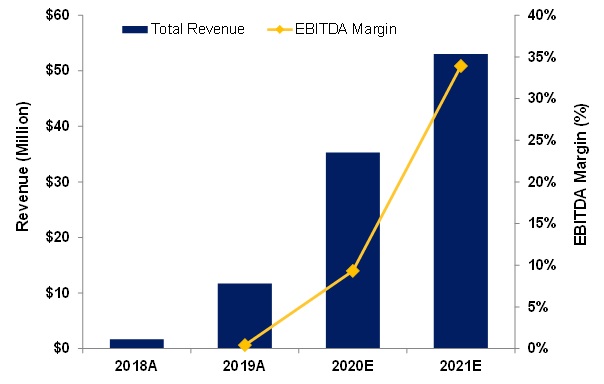

- Peak’s revenue in 2019 was $11.7 million compared to $1.7 million in 2018.

- Revenue for 2019 was slightly lower than our estimate of $12.1 million. The increase in revenue during the year was attributed to new service offerings from the Company’s ASDS, ASCS and ASSC subsidiaries, accounting for $8.3 million of new revenue since these subsidiaries did not exist or generate revenue in 2018.

- In 2019, subsidiary ASFC generated revenue of $3.4 million, up from $1.7 million in 2018.

- ASFC was established in April 2018, so 2019 was ASFC’s first full year of operations.

- COVID-19 Impact:

- Peak experienced a decline in revenue in Q1 & Q2/2020 based on the negative impact of the coronavirus on business in China. Peak‘s ASSC subsidiary resumed operations on February 24 and the Company expects a return to normal business operations in China in Q2/2020. We have adjusted our Q1 & Q2/2020 revenues lower but maintain our 2020 revenue estimate.

- Peak could benefit as the Company announced that their Cubeler Lending Hub platform would be used to help distribute government relief funds to small and medium sized businesses that were affected by the coronavirus.

- Upcoming Catalyst:

- Peak leveraging the newly acquired Jinxiaoer platform to expand its services to new cities & signing new banks to the lending network.

FINANCIAL ANALYSIS & VALUATION:

- We modelled Peak’s revenue for 2020-2022 as a sum of the revenue from the six operating subsidiaries and estimated:

- 2020: Revenue $35.3 million; EBITDA $3.3 million;

- 2021: Revenue $53.1 million; EBITDA $18.0 million;

- 2022: Revenue $58.4 million; EBITDA $22.4 million.

- Using a revenue multiple of 4x 2020 Revenue, an EBITDA multiple of 10x 2020 EBITDA, and a DCF at 10%, we estimate an equal-weighted price per share target of $0.19.

- We are maintaining a “Buy” rating and One-year Target Price of $0.20.

//

You can download our 14-page Update Report by clicking on the following link: eR-Peak_PKK-UR-2020_05_31-FINAL

//

CHART 1: Revenue and EBITDA Margins – Actuals & Estimates – 2019-2021