eResearch | This week, major Canadian banks reported Q2/2020 earnings, with profits across most banks decreasing between 30-70% due to the pandemic significantly increasing Provisions for Credit Losses (“PCL”) on impaired and performing loans.

In 2014, the IASB completed its response to the previous financial crisis with a change from standards IAS 39 to IFRS 9, which enforced banks to promptly report loan and credit loss provisions, in addition to clearly outlining balance sheet items.

Banks such as Toronto-Dominion Bank (TSX: TD), who have a strong focus on consumer and commercial banking, were hit the hardest by the pandemic, with the highest levels of total PCL on loans. Nevertheless, all banks are significantly increasing PCL on performing loans due to deteriorating economic outlooks.

See below for further details on Q2/2020 earnings and PCL on loans for all major Canadian banks.

BMO

![]()

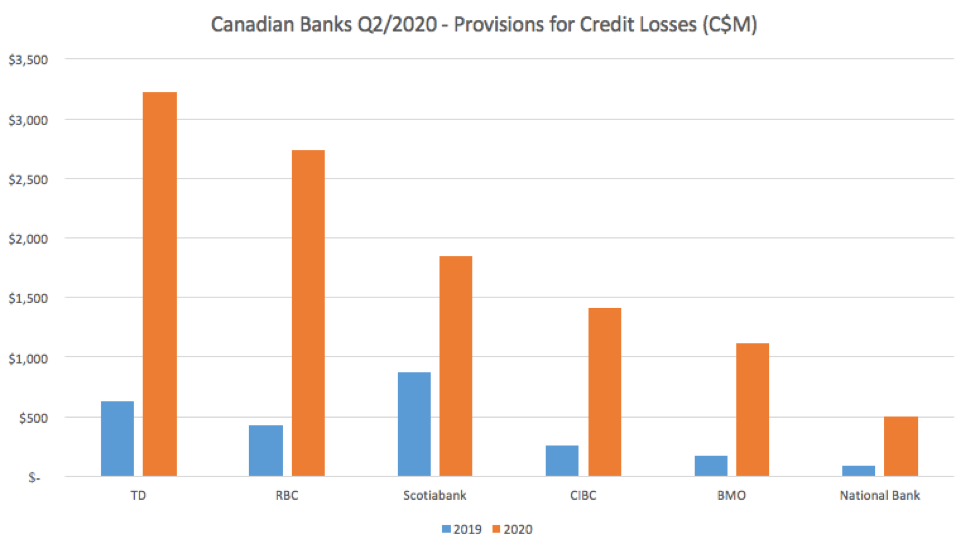

![]() In Q2/2020, Bank of Montreal (TSX: BMO) reported total PCL on loans of C$1.1 billion, a 535% increase year-over-year, which included PCL on impaired loans of C$413 million, a 175% increase year-over-year, and PCL on performing loans of C$705 million, a 2,611% increase year-over-year.

In Q2/2020, Bank of Montreal (TSX: BMO) reported total PCL on loans of C$1.1 billion, a 535% increase year-over-year, which included PCL on impaired loans of C$413 million, a 175% increase year-over-year, and PCL on performing loans of C$705 million, a 2,611% increase year-over-year.

The higher provision for credit losses on impaired loans was mainly due to deterioration in BMO’s Personal and Commercial banking division and Capital Markets division. The increased provision for credit losses on performing loans was primarily due to a weaker economic outlook.

BMO’s top and bottom line both decreased due to the pandemic impacting all business divisions. BMO’s PCL to average net loans and acceptances increased to 0.94% compared with 0.16% in the prior year, which included a large recovery from a U.S. commercial loan.

In the earnings report, BMO’s CEO, Darryl White, stated, “We have a strong capital and liquidity position, a disciplined operating plan and very good momentum. The strength and resilience of our overall diversified business model has been tested and we are performing well through these challenges. As a result, I’m confident that our Bank has never been positioned better to face the environment ahead.”

BMO Q2/2020 Financial Highlights

- Revenue of C$5.3 billion, a 15% decrease year-over-year.

- Net income of C$689 million, a 54% decrease year-over-year.

- Balance Sheet consists of Cash and cash equivalents of C$72 billion, Deposits of C$7.7 billion, Securities of C$214 billion, and Loans of C$472 billion.

- ROE of 5.3% compared with 14% in the prior year.

- CET1 Ratio of 11%, above regulatory requirements.

CIBC

![]()

![]() In Q2/2020, the Canadian Imperial Bank of Commerce (TSX: CM) reported total PCL on loans of C$1.4 billion, a 441% increase year-over-year, which included PCL on impaired loans of C$343 million, a 37% increase year-over-year, and PCL on performing loans of C$1.1 billion, a 450% increase year-over-year.

In Q2/2020, the Canadian Imperial Bank of Commerce (TSX: CM) reported total PCL on loans of C$1.4 billion, a 441% increase year-over-year, which included PCL on impaired loans of C$343 million, a 37% increase year-over-year, and PCL on performing loans of C$1.1 billion, a 450% increase year-over-year.

The higher provision for credit losses on impaired loans was mainly due to deterioration in CIBC’s Canadian Commercial Banking & Wealth Management division and Capital Markets division. The increased provision for credit losses on performing loans was primarily due to higher risks from economic uncertainty.

Though CIBC reported positive revenue growth, it struggled to maintain profits as provisions for credit losses were significantly increased across all small business divisions due to the pandemic. CIBC’s PCL to average net loans and acceptances increased to 1.19% compared with 0.26% in the prior year.

In the earnings report, CIBC’s CEO, Victor Dodig, stated, “Our capital position remains strong, giving us flexibility and resilience as we navigate the current environment and continue to advance our long-term client-focused strategy”

CIBC Q2/2020 Financial Highlights

- Revenue of C$4.6 billion, a 1% increase year-over-year.

- Net income of C$392 million, a 71% decrease year-over-year.

- Balance Sheet consists of Cash and cash equivalents of C$38 billion, Deposits of C$18 billion, Securities of C$134 billion, and Loans of C$412 billion.

- ROE of 4% compared with 16% in the prior year.

- CET1 Ratio of 11%, above regulatory requirements.

National Bank

![]()

![]() In Q2/2020, National Bank of Canada (TSX: NA) reported total PCL on loans of C$504 million, a 500% increase year-over-year, which included PCL on impaired loans of C$113 million, a 34% increase year-over-year, and PCL on performing loans of C$391 million, compared with none in the prior year.

In Q2/2020, National Bank of Canada (TSX: NA) reported total PCL on loans of C$504 million, a 500% increase year-over-year, which included PCL on impaired loans of C$113 million, a 34% increase year-over-year, and PCL on performing loans of C$391 million, compared with none in the prior year.

The higher provision for credit losses on impaired loans was attributed to all of National Bank’s business divisions, while increased provisions for credit losses on performing loans were primarily driven from the Commercial banking division and the Financial Markets division.

Though the pandemic significantly increased National Bank’s provisions for credit losses, revenue experienced growth, especially within its Financial Markets division, which grew revenue by 83% year-over-year. National Bank’s PCL to average net loans and acceptances increased to 1.28% compared with 0.23% in the prior year.

In the earnings report, National Bank’s CEO, Louis Vachon, stated, “I am confident that the resilience of the bank’s franchise, our defensive positioning, the quality of our credit portfolios, and our strong balance sheet will serve us well as we manage through these uncertain times.”

National Bank Q2/2020 Financial Highlights

- Revenue of C$2 billion, a 15% increase year-over-year.

- Net income of C$379 million, a 32% decrease year-over-year.

- Balance Sheet consists of Cash and Deposits of C$28 billion, Securities of C$85 billion, and Loans of C$157 billion.

- ROE of 11% compared with 18% in the prior year.

- CET1 Ratio of 11%, above regulatory requirements.

RBC

![]()

![]() In Q2/2020, Royal Bank of Canada (TSX: RY) reported total PCL on loans of C$2.8 billion, a 542% increase year-over-year, which included PCL on impaired loans of C$613 million, a 41% increase year-over-year, and PCL on performing loans of C$2.1 billion, a 575% increase year-over-year.

In Q2/2020, Royal Bank of Canada (TSX: RY) reported total PCL on loans of C$2.8 billion, a 542% increase year-over-year, which included PCL on impaired loans of C$613 million, a 41% increase year-over-year, and PCL on performing loans of C$2.1 billion, a 575% increase year-over-year.

The higher provision for impaired loans was mainly due to RBC’s Capital Markets division, while increased provisions for credit losses on performing loans primarily came from divisions including Personal & Commercial Banking and Wealth Management.

Though the pandemic significantly impacted RBC’s bottom line, it was slightly offset by increased revenues from Investor & Treasury Services and Insurance divisions. RBC’s PCL to average net loans and acceptances increased to 1.65% compared with 0.29% in the prior year.

In the earnings call, RBC’s CEO, David McKay, stated, “We will continue to leverage our strong balance sheet, our leading scale and distribution capabilities across our franchises to prudently and efficiently support our clients. And we believe our past investments in building unique capabilities such as Borealis AI, Insight Edge and MyAdvisor will significantly differentiate us in the future and enable us to deliver even more value for our clients.”

RBC Q2/2020 Financial Highlights

- Revenue of C$10.3 billion, a 10% decrease year-over-year.

- Net income of C$1.5 billion, a 54% decrease year-over-year.

- Balance Sheet consists of Cash and cash equivalents of C$99 billion, Deposits of C$48 billion, Securities of C$270 billion, and Loans of C$679 billion.

- ROE of 7.3% compared with 18% in the prior year.

- CET1 Ratio of 12%, above regulatory requirements.

Scotiabank

![]()

![]() In Q2/2020, Bank of Nova Scotia (TSX: BNS) reported total PCL on loans of C$1.8 billion, a 111% increase year-over-year, which included PCL on impaired loans of C$870 million, a 24% increase year-over-year, and PCL on performing loans of C$976 million, a 43% increase year-over-year.

In Q2/2020, Bank of Nova Scotia (TSX: BNS) reported total PCL on loans of C$1.8 billion, a 111% increase year-over-year, which included PCL on impaired loans of C$870 million, a 24% increase year-over-year, and PCL on performing loans of C$976 million, a 43% increase year-over-year.

Scotiabank’s increase in credit losses on impaired loans was mainly due to the Canadian Banking, International Banking, and Global Banking and Markets divisions. The increased provision for credit losses on performing loans was primarily due to unfavourable macroeconomic outlooks.

Though Scotiabank’s bottom line deteriorated significantly, it posted growth in revenues, primarily due to a 25% increase in the Global Wealth Management division. Scotiabank’s PCL to average net loans and acceptances increased to 1.19% compared with 0.61% in the prior year.

In the earnings call, Scotiabank’s CEO, Brian Porter, stated “We continue to provision early and conservatively. Our asset quality remains strong with high levels of secured and investment-grade assets. We are also highly diversified by product, by sector and by geography”.

Scotiabank Q2/2020 Financial Highlights

- Revenue of C$7.96 billion, a 2% increase year-over-year.

- Net income of C$1.3 billion, a 41% decrease year-over-year.

- Balance Sheet consists of Cash and Non-interest-bearing deposits of C$12 billion, Interest-bearing deposits of C$92 billion, Securities of C$121 billion, and Loans of C$631 billion.

- ROE of 7.9% compared with 14% in the prior year.

- CET1 Ratio of 11%, above regulatory requirements.

TD

![]()

![]() In Q2/2020, Toronto-Dominion Bank (TSX: TD) reported total PCL on loans of C$3.2 billion, a 408% increase year-over-year, which included PCL on impaired loans of C$967 million, a 63% increase year-over-year, and PCL on performing loans of C$3.2 billion, a 408% increase year-over-year.

In Q2/2020, Toronto-Dominion Bank (TSX: TD) reported total PCL on loans of C$3.2 billion, a 408% increase year-over-year, which included PCL on impaired loans of C$967 million, a 63% increase year-over-year, and PCL on performing loans of C$3.2 billion, a 408% increase year-over-year.

TD’s higher provision for impaired loans was due to credit migration in Wholesale Banking, in addition to deterioration in Consumer and Commercial lending portfolios. The increased provision for credit losses on performing loans was primarily due to heightened uncertainties in the economic outlook.

Though TD was hit significantly hard in its retail business divisions, it was partially offset by higher revenues and lower non-interest expenses. TD’s PCL to average net loans and acceptances increased to 1.76% compared with 0.39% in the prior year.

In the earnings report, TD’s CEO, Bharat Masrani, stated, “TD entered this operating environment from a position of strength, with a high quality balance sheet and strong liquidity and capital positions. The Bank will continue to help our customers, colleagues and communities as we work to recover from the current crisis and work with governments, regulators and other stakeholders to rebuild our economies,”

TD Q2/2020 Financial Highlights

- Revenue of C$10.2 billion, a 3% increase year-over-year.

- Net income of C$1.5 billion, a 52% decrease year-over-year.

- Balance Sheet consists of Cash and due from banks of C$5.3 billion, Deposits of C$147 billion, Securities of C$339 billion, and Loans of C$754 billion.

- ROE of 6.9% compared with 17% in the prior year.

- CET1 Ratio of 11%, above regulatory requirements.

//

CHART 1: S&P 500 vs BMO, BNS, CM, NA, RY, and TD – 1 Year Stock Performance