On May 4, 2020, Ralph Garcea of Focus Merchant Group (FMG), formerly the Tech Analyst at Echelon Wealth Partners, issued an updated research report on Quisitive Technology Solutions (“Quisitive”, TSXV: QUIS).

Quisitive is a premier Microsoft solutions provider that helps enterprise organizations move, operate and innovate in the Microsoft cloud, serving clients globally with offices in Dallas (TX), Denver (CO) and Toronto, Ontario.

Quisitive Q4/2019 Results & Outlook; Microsoft FQ3/20 Shows Multiple Surges

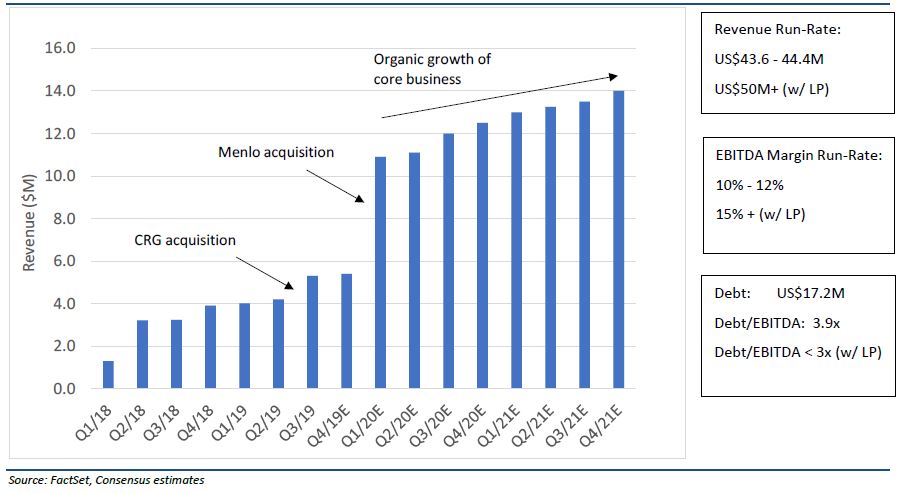

- Quisitive reported 2019 Revenue of $18.5 million (+47% Y/Y), with Gross Margins of $7.9 million (43% margin) and adjusted EBITDA of $1.3 million (7% of Revenue). For Q4/2019, revenue $5.4 million (Consensus: $5.5 million) (+39% Y/Y), with Gross Margins of $2.3 million (43% margin) and adjusted EBITDA of $0.78 million (14.5% margins) (Consensus: $0.6 million) (excluding discretionary bonus expense of $0.46 million). There was no revenue contribution from Menlo in Q4/2019.

- Quisitive provided positive preliminary Q1/2020 guidance for revenue of approximately $10.9–11.1 million (Consensus: $10.0 million), Gross Margins of approximately $4.1–4.3M, and adjusted EBITDA of approximately $1.0-1.2 million (Consensus: $1.4 million). This includes Menlo, but no LedgerPay Revenue, which should start ramping in Q2/2020 (all values in US$ unless otherwise noted).

- Microsoft reported FQ3/2020 revenue of $35.0 billion (+15% Y/Y) (Consensus: $33.8 billon), and EPS of $1.40 (+23% Y/Y) (Consensus: $1.27). Azure revenue grew 59% Y/Y (+61% in constant currency). CEO Satya Nadella commented on seeing “two years’ worth of digital transformation in two months” and helping customers adapt to “a world of remote everything”.

- In this note, we also look at the continuing cloud war between Microsoft Azure and Amazon AWS, and how much the two combatants are spending on capex to keep up with the secular surge in demand.

Revenue Estimates Show CRG and Menlo Impact on Quisitive Quarterly Revenues (Without Revenue Synergies or LedgerPay)

Catalysts for Growth

- We expect more LedgerPay announcements as Quisitive works through its pipeline. Future deals could be a mix of SaaS-based revenue and annual license with maintenance and support.

- Quisitive will report Q1/20 results towards the end of May.

Valuation:

- Ralph Garcea continues to believe that Quisitive is undervalued as, on a consensus basis, trades at an EV/Sales and EV/EBITDA of 2.4x/17.2x (fully diluted) versus its North American IT Services and Global Payment Technology comparables trading at 1.5x/11.1x and 5.5x/14.0x, respectively.

- He believes Quisitive’s consulting business should trade in-line with IT Services companies at 1-1.5x EV/Sales, and 10-12x EV/EBITDA, and LedgerPay should trade in-line with Fin Tech companies at 5-6x EV/Sales, and 13-15x EV/EBITDA.

- Using a sum-of-the-parts calculation on 2021E estimates for Quisitive, yields a valuation in the $0.73-1.46 range (vs. $0.69-1.41 previous).

You can access the report at the following link: FMG Research_QUIS_May042020

//

Quisitive Technology Solutions (TSXV:QUIS )

- quisitive.com

- Headquartered in Toronto, Canada, Quisitive Technology Solutions provides Microsoft solutions, primarily in North America, offering Microsoft cloud assessment & solution services, migration and implementation, as well as application maintenance, configurations, upgrading, performance analytics and intelligence.

- Quisitive offers cloud solutions for CRM, healthcare, manufacturing, oil and gas, payments, and supply chain industries.

- Quisitive Technology Solutions is currently trading at $0.75 with a market cap of $83.9 million.

//