eResearch | A Financial Sense article, authored by Adam Rozencwajg, looks at the current low cost of commodities, why they are at these low levels, and what impact these could have on the market. He zeroes in on one particular commodity that he thinks is particularly under-valued in the current market context.

Mr. Rozencwajg is a founding partner of Goehring & Rozencwajg, an investment firm focused on natural resources. He has nine years of investment experience, including working exclusively with Mr. Goehring on the Global Natural Resources Fund at Chilton Investment Company between 2007 and 2015.

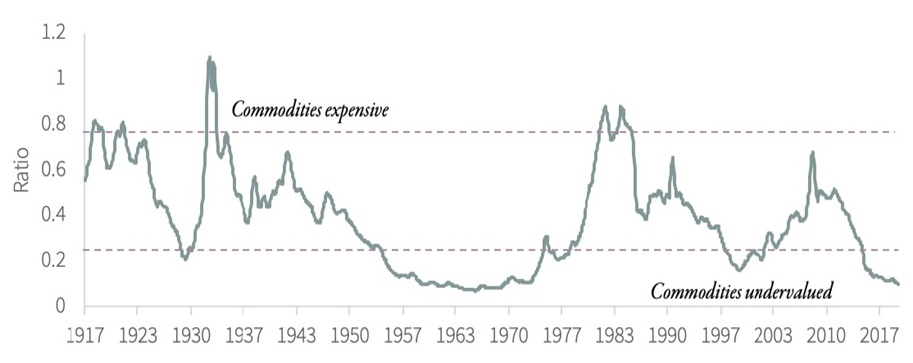

Natural Resource Stocks Are Cheap

In his efforts to identify the over-looked potential of natural resource companies, the Author has determined that commodities are substantially undervalued as an asset class and are cheap relative to other financial assets. He illustrates this in the following chart.

Commodity Index versus Dow Jones Industrial Average

Investors fully realize that commodities have been in a bear market for more than 10 years. However, historically, whenever commodity prices became substantially under-valued, as they are now, relative to stock prices, it has proven to be an opportune time to invest directly in commodities.

The author provides three examples of this occurrence, being in (1) 1929 (just before the Great Depression), (2) 1969 (just before the wild inflationary period that dominated the 1970s), and (3) 1999 (just before the dot.com bubble). He believes that the most recent occurrence is right now.

Largest Under-Valued Commodity: Oil

Although the price of oil reached its recent low in February 2016, many energy stocks continue to achieve new record lows. Mr. Rozencwajg believes that current energy prices are too low to balance global demand and supply. Nonetheless, he is bullish on the demand side of the equation, while the price of oil is considered to be too low to provide any incentive to raise production in order to improve supply.

Shale Oil Impact Lessening

Adding to the longer-term bullish outlook for energy resources is the incremental decline in shale oil output. Depletion rates now seem to be accelerating. The three major U.S. shale-oil basins are possibly past their prime and there are no new major shale oil areas on the horizon.

Market Implications

All of this means that any excess supply is likely to wane over time and, therefore, bring the demand/supply equation back towards balance. This would have a salutatory effect on energy stock prices.

You can read the entire Financial Sense article by clicking the following link:

https://www.financialsense.com/blog/19357/adam-rozencwajg-commodities-are-radically-undervalued

//